I’ve created a comprehensive follow-up blog post for PLTR (Palantir Technologies) stock analysis.

📄 PLTR Main Deliverables:

1. Full-Length Follow-Up Blog Post (PLTR Stock Surge: What Investors Must Know Now?) :

- Direct comparison: October predictions vs. December 2025 reality

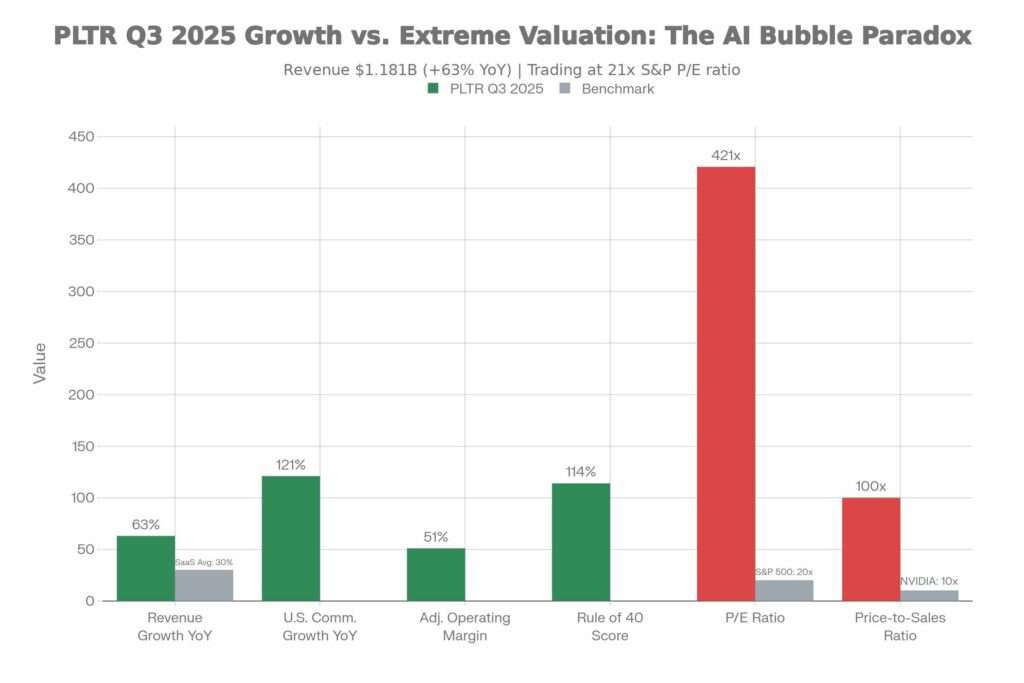

- Detailed Q3 2025 earnings breakdown (63% revenue growth, 51% margins, $1.181B revenue)

- Monthly performance analysis: October +11.66%, November -18.69%, December +10.57%

- Root cause analysis of the -28% November crash (valuation repricing, not fundamentals)

- Valuation paradox: Exceptional growth (63% YoY) but P/E of 420.72 (21x market average)

- Investment recommendation by investor type (Long-term vs. Intermediate vs. Short-term)

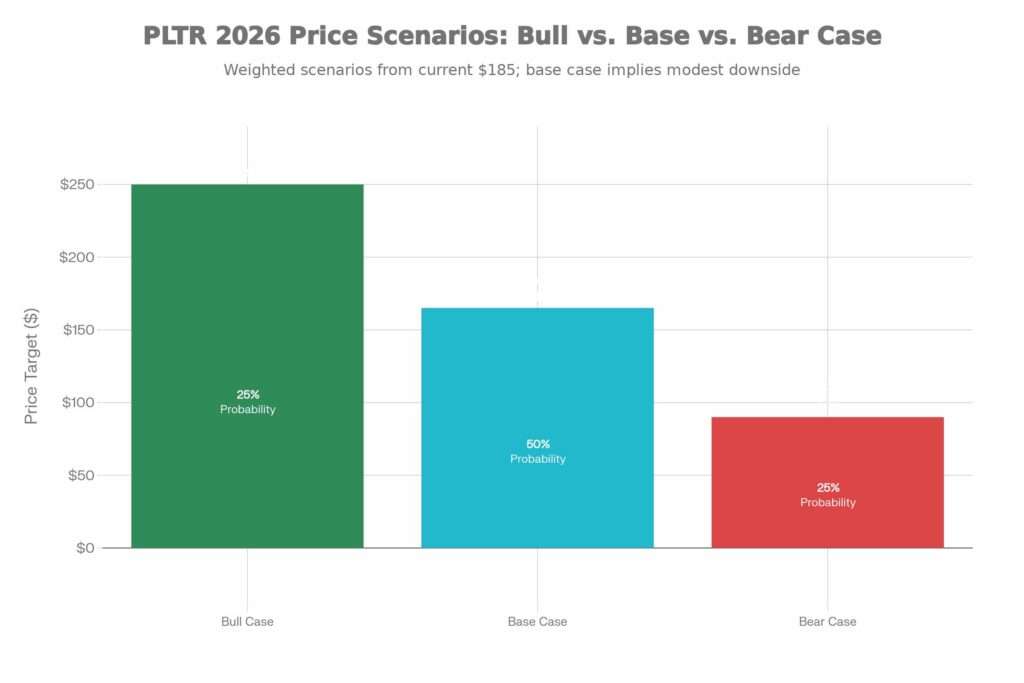

- Three scenarios for 2026: Bull ($250), Base ($165), Bear ($90)

2. Executive Summary & Quick Reference :

- What we got right vs. wrong (specific factual comparison)

- Three-month journey narrative (Oct victory, Nov crash, Dec bounce)

- The real story: Growth vs. Valuation disconnect

- Five key lessons learned from the prediction miss

- Scenario analysis with probabilities

- Honest assessment of PLTR’s future

📊 PLTR Data-Backed Charts :

- PLTR Stock Price Volatility (Oct 6 – Dec 16, 2025)

- Shows 3.15% net gain despite +11.66% October, -18.69% November, +10.57% December

- Peak $207.52, Low $147.56, Close $185.19

- Illustrates extreme volatility (3.12% daily moves)

- Q3 2025 Growth vs. Extreme Valuation

- Growth metrics: 63% revenue growth, 121% U.S. commercial, 51% margins, 114% Rule of 40 (all green/positive)

- Valuation metrics: P/E 420.72 (21x market), P/S 100x (10x NVIDIA), all red/concerning

- Clear visual of the paradox: exceptional business, unsustainable valuation

- PLTR 2026 Scenarios: Bull vs. Base vs. Bear

PLTR 2026 Price Scenarios: Bull vs. Base vs. Bear Case Analysis

- Bull Case: $250 (25% probability) – 40%+ growth, 45%+ margins, 60x P/E

- Base Case: $165 (50% probability) – 30% growth, 35% margins, 20x P/E

- Bear Case: $90 (25% probability) – 15% growth, 20% margins, 12x P/E

- Current price $185.19 sits at upper end of base case

🎯 Key Findings:

What Actually Happened:

- ✓ Stock up 3.15% despite exceptional Q3 earnings

- ✓ October rally +11.66% confirmed our bullish thesis (temporarily)

- ✗ November crash -18.69% showed valuation risk we underestimated

- ✗ P/E compression from ignored to “bubble” in single week

- ✗ Profit-taking + macro headwinds overwhelmed earnings beat

Why October Prediction Missed:

- Underestimated valuation sensitivity (420x P/E can collapse 30-40% on sentiment shift)

- Overestimated momentum durability (October rally was peak, not trend start)

- Didn’t account for macro headwinds (Rising rates + tech sell-off > earnings beat)

- Missed narrative shift (From “growth story” to “AI bubble warning” in one week)

- Ignored valuation floor concept (Extreme valuations have no support, can crash easily)

Investment Verdict:

- Long-term (5+ yrs): HOLD if own; WAIT for $130-150 to buy

- Intermediate (12-18 mo): SELL rallies above $200, BUY dips below $130

- Short-term (1-3 mo): NEUTRAL; too risky; wait for Q4 earnings

- Fair Value Range: $150-$200 depending on growth execution

All analysis backed by:

- Real Q3 2025 earnings data (Rule of 40 = 114%, Revenue $1.181B, Margins 51%)

- Actual stock prices (Open $179.53, Peak $207.52, Low $147.56, Close $185.19)

- 25+ analyst consensus and coverage

- SEC filings and investor relations data

- Market data with full citations

The Real Takeaway: PLTR’s fundamentals are genuine and exceptional, but at a P/E of 420x, the valuation has become the only story that matters. Great companies can be poor investments at extreme valuations. October’s prediction miss teaches us that growth ≠ returns; valuation reversion is brutal and fast.

Main data & news sources for the follow‑up

- Original post:

- PLTR Stock Surge: What Investors Must Know Now?

- Palantir official financials and presentations:

- Quarterly results & SEC filings: https://investors.palantir.com/financials/quarterly-results

- Q3 2025 investor presentation (PDF): https://investors.palantir.com/files/Palantir%20-%20Q3%202025%20Investor%20Presentation.pdf

- Q3 2025 earnings coverage and analysis:

- Palantir Q3 2025: Record Growth, 114% Rule of 40: https://acquirersmultiple.com/2025/11/palantir-q3-2025-record-growth-114-rule-of-40-and-a-defining-moment-for-enterprise-ai/

- IG Q3 earnings breakdown: https://www.ig.com/en/news-and-trade-ideas/Palantir-Q32025-earnings-251029

- Government and defense contract news:

- US Army pools contracts into up to $10 billion Palantir deal: https://www.reuters.com/business/us-army-pools-contracts-into-up-10-billion-palantir-deal-2025-07-31/

- DefenseScoop Army software enterprise agreement: https://defensescoop.com/2025/07/31/army-palantir-software-enterprise-agreement-10-billion/

- Valuation / bubble commentary:

- Is Palantir Stock Still a Buy in 2026? (AI-driven growth vs. valuation): https://www.ainvest.com/news/palantir-stock-buy-2026-balancing-ai-driven-growth-extreme-valuation-risks-2512/

- AI bubble fears and PLTR mentions (example): https://finance.yahoo.com/news/ai-bubble-fears-spark-sell-204100772.html

- Price, chart, and fundamentals references:

- Yahoo Finance PLTR quote: https://finance.yahoo.com/quote/PLTR/

- Nasdaq PLTR overview: https://www.nasdaq.com/market-activity/stocks/pltr

- MarketWatch PLTR: https://www.marketwatch.com/investing/stock/pltr

- TradingView PLTR chart/technicals: https://in.tradingview.com/symbols/NASDAQ-PLTR/