BAC looks well-positioned for 2025. Earnings re-accelerated on strong investment banking activity, record net interest income, and disciplined costs. Moreover, analysts now see mid-teens upside over 12 months while credit metrics remain stable. Additionally, valuation sits near fair, yet improving fee momentum and a clearer rate path can unlock more gains. However, this is analysis, not advice. And, because markets change fast, you should always do your own research before acting on any idea.

Disclaimer: This is only analysis. We do not encourage you to buy, sell, or hold. Markets change. Please do your own due diligence.

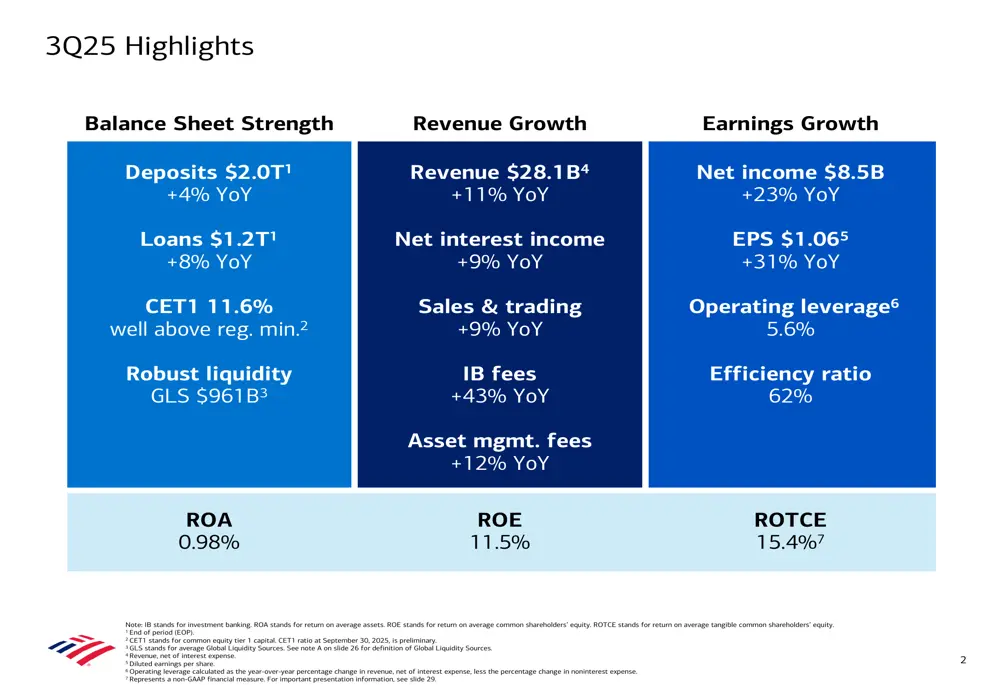

2025 Snapshot: What Stands Out Now

BAC’s third quarter showed powerful operating leverage. Revenue grew double digits, and net income jumped more than 20%, which signals broad-based momentum across investment banking, trading, and lending. Furthermore, record net interest income and a stronger fee mix underline improving quality of earnings. Therefore, with consensus price targets implying additional upside, the stock offers a balanced risk-reward for long-term investors who prefer large-cap banks with scale and diversification.

BAC Fundamentals: Earnings, Revenue, and Profit Drivers

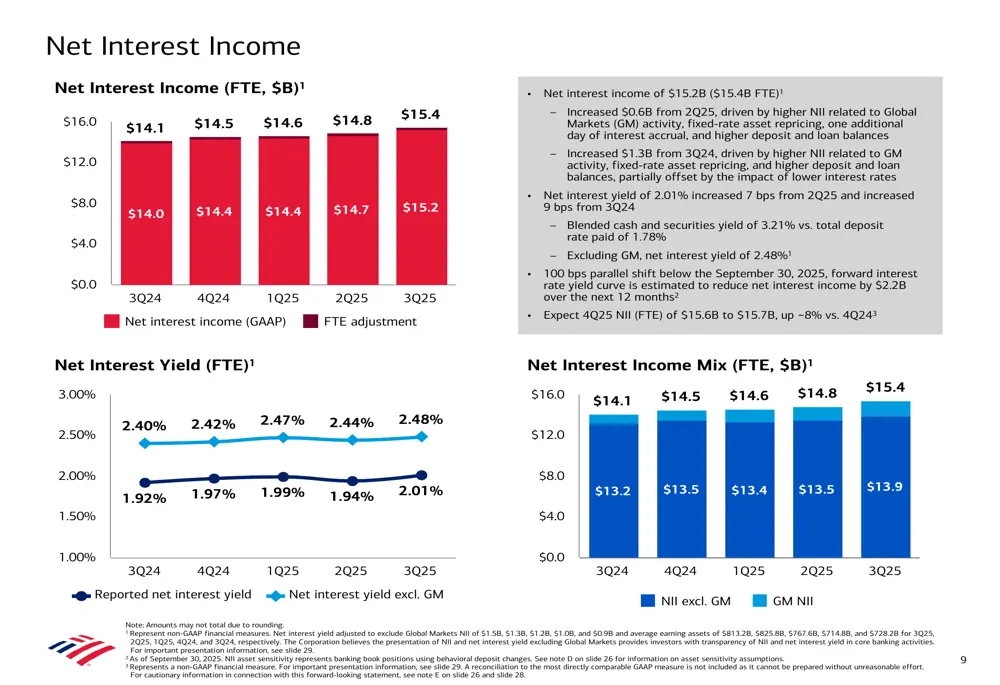

As rates normalized and capital markets reopened, BAC’s fee engine fired up. Investment banking fees rose 43% year-over-year, while equities and fixed income trading beat estimates. Meanwhile, net interest income hit a record, supported by loan growth, better deposit mix, and asset repricing. Consequently, the bank posted meaningful gains in EPS and return ratios. Thus, profitability was not only higher but also more durable due to improved business mix.

Return metrics offer further comfort. ROE in the low double digits and ROTCE in the mid-teens show BAC is compounding value efficiently. Additionally, management emphasized operating leverage and efficiency ratio improvement, which helps earnings resilience if growth moderates. Therefore, even as competition intensifies, BAC’s scale and balanced model support steady compounding potential.

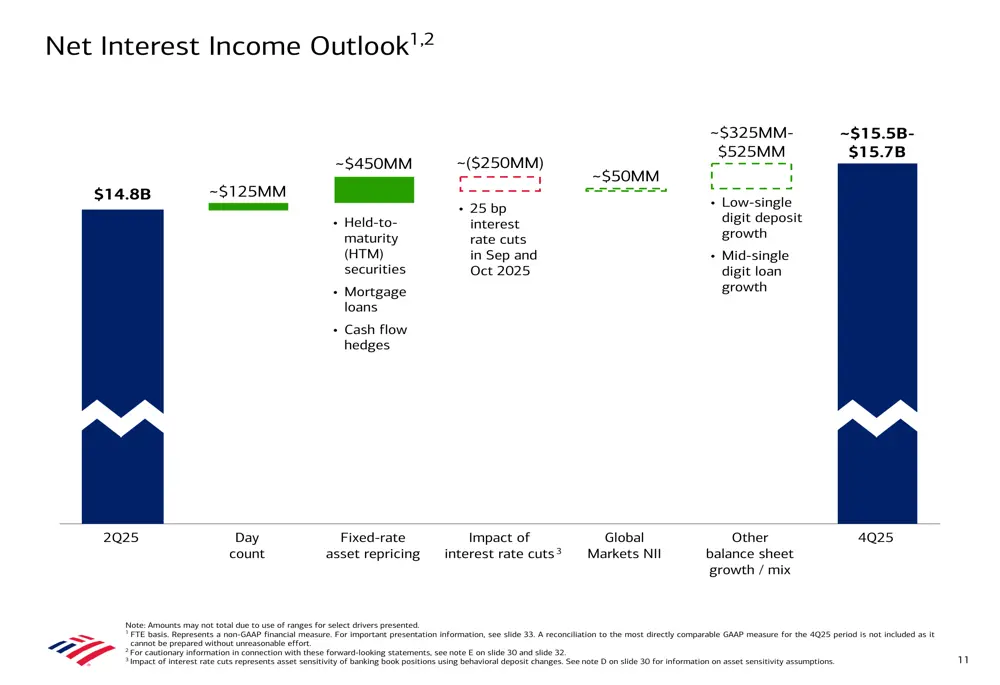

BAC Net Interest Income: What Rate Cuts Mean Next

Because BAC is interest-rate sensitive, small policy shifts matter. Management expects Q4 net interest income around $15.5–$15.7 billion, even after factoring recent 25 bps rate cuts. However, ongoing asset repricing, loan growth, and deposit optimization should offset some headwinds. Therefore, despite slight pressure from lower rates, the trajectory into Q4 still points higher due to balance sheet mix and maturities rolling into better yields.

BAC Fee Engines: Dealmaking and Wealth Are Back

Capital markets thawed, and dealmaking surged, which revived high-margin fee pools across Wall Street. BAC benefited as activity in M&A, equity issuance, and financing rose. Moreover, sales and trading delivered healthy gains with ongoing client demand. Additionally, wealth and asset management posted double-digit growth in fees, which helps diversify revenue and stabilize earnings through cycles. Hence, multiple engines now pull forward together, which is a key quality signal for large banks.

BAC Balance Sheet Strength: Deposits, Loans, Capital, Liquidity

BAC’s balance sheet remains robust. Deposits grew year-over-year, loans expanded at a solid pace, and capital ratios stayed well above regulatory minimums. Moreover, liquidity buffers are deep, which builds confidence in the bank’s ability to navigate uncertainty. Furthermore, management’s focus on high-quality underwriting and disciplined risk culture supports benign credit costs. Therefore, even with macro swings, BAC looks well-prepared to defend earnings and fund growth.

BAC Valuation and Targets: Is There Room to Run?

Sell-side targets cluster around the mid-50s over the next year. The consensus suggests high single-digit to mid-teens upside, with the spread explained by differing views on rates, fee momentum, and credit costs. Nevertheless, the majority skew Buy to Moderate Buy. Given stronger revenue breadth and record NII, a modest valuation re-rating could follow if execution remains consistent. However, the path depends on macro stability and continued dealmaking strength.

BAC Chart Analysis: Trend, Levels, and Momentum

Technically, BAC’s multi-month trend reflects improved earnings visibility and a healthier macro backdrop. After testing resistance near its 52-week high, the stock saw a standard pullback alongside headline volatility. However, supports near prior breakout zones often attract buyers, particularly when earnings momentum is intact. Therefore, if price holds above the 200-day moving average and breadth remains firm, risk-reward can favor a gradual grind higher.

BAC Dividends, Buybacks, and Income Appeal

For income-focused investors, BAC’s dividend yield sits in a competitive range for large-cap financials. Moreover, payout ratio remains manageable, which gives room for steady increases if earnings compound. Additionally, buybacks can enhance per-share growth when trading near fair value. Therefore, for those building core financial exposure, BAC offers a blend of income, quality, and scale. However, always assess dividend sustainability versus your own risk tolerance.

What Could Go Wrong: Key Risks to Watch

Banks are cyclical, so earnings remain sensitive to growth and credit. A sharper economic slowdown could pressure loan demand, fee activity, and asset quality. Additionally, more aggressive rate cuts could compress net interest margins faster than expected. Furthermore, regulatory shifts might raise capital or liquidity requirements. Therefore, investors should watch consumer deposits, commercial credit quality, and trading conditions each quarter to calibrate conviction.

How to Think About BAC for Different Investors

- For long-term builders: BAC’s scale, diversified fees, and improving efficiency make it a credible core holding candidate. However, stagger entries to manage volatility risk.

- For dividend seekers: The combination of yield, buybacks, and operating leverage can support total returns. Nevertheless, watch NII trends and credit provisioning closely.

- For growth-tilted investors: The investment banking and trading upcycle could continue if corporate confidence holds. Therefore, fee upside becomes a key swing factor this year.

Final Word: Balanced, Data-Led, and Patient

In plain words, BAC’s story today is about balance. Earnings are rising across multiple engines, capital is strong, and valuation is reasonable. Moreover, management is delivering operating leverage while protecting credit quality. However, macro surprises can still swing sentiment. Therefore, patience, risk controls, and periodic check-ins on NII, fees, and credit will matter most in 2025. And, as always, please treat this as analysis, not advice—and do your own due diligence before acting.

👉 You Might also find this post insightful – https://bosslevelfinance.com/how-jmp-is-winning-in-the-financial-sector-now

👉 Create a Vested Account today to start investing in US Stocks – https://refer.vestedfinance.com/RUKU88007

Sources: stock analysis portals and price pages with fundamentals and targets; major financial news outlets; official company investor materials and earnings presentations

- https://www.cnbc.com/2025/10/15/bank-of-america-bac-earnings-q3-2025.html

- https://www.marketbeat.com/stocks/NYSE/BAC/forecast/

- https://www.reuters.com/business/finance/bank-america-profit-rises-investment-banking-strength-2025-10-15/

- https://www.marketwatch.com/story/bank-of-america-rides-a-43-jump-in-investment-banking-revenue-to-a-big-profit-beat-dff86a58

- https://www.wsj.com/finance/banking/bank-of-america-bac-q3-earnings-report-stock-2025-6af3d29d

- https://www.theglobeandmail.com/investing/markets/stocks/BAC/pressreleases/35512044/bank-of-america-earnings-call-highlights-robust-growth/

- https://finance.yahoo.com/news/wall-street-boom-boosts-profits-at-bank-of-america-morgan-stanley-114911558.html

- https://stockanalysis.com/stocks/bac/forecast/

- https://www.tipranks.com/stocks/bac/forecast

- https://www.cnbc.com/quotes/BAC

- https://investor.bankofamerica.com/shareholder-information/historical-data

- https://stockanalysis.com/stocks/bac/

- https://in.investing.com/equities/bank-of-america-consensus-estimates

- https://finance.yahoo.com/research/stock-forecast/BAC/

- https://finance.yahoo.com/quote/BAC/

- https://newsroom.bankofamerica.com/content/newsroom/press-releases/2025/10/bank-of-america-announces-redemption-of–1-750-000-000-1-949–fi.html

- https://in.tradingview.com/symbols/NYSE-BAC/forecast/

- https://coincodex.com/stock/BAC/price-prediction/

- https://public.com/stocks/bac/forecast-price-target

- https://www.cnn.com/markets/stocks/BAC