Meta just reported a milestone quarter, with revenue of about 56.3 billion, up roughly 33% year on year. Advertising sales drove almost all of this, with ad revenue also growing by about 33% and ad impressions rising 19 % while the average price per ad increased 12%. Operating margin stayed around 41%, and because cost of revenue was only about 10.2 billion, the implied gross margin is close to 82%, which is elite for a large‑cap tech name.

However, despite these strong numbers, management raised its 2026 capital‑expenditure guidance to a range of about 125 to 145 billion, up from a previous range near 115 to 135 billion, mainly to fund AI infrastructure and data centers. As a result, the stock dropped sharply in after‑hours and pre‑market trading, even though the headline results were ahead of many expectations. In simple words, the market loved the profits but panicked about the bill for the next wave of growth.

Core business check: is meta’s ad engine still healthy?

First, let us look at the engine that pays for everything. The family of apps segment, which includes Facebook, Instagram, WhatsApp and Messenger, generated about 55.9 billion in revenue this quarter. Out of that, advertising contributed roughly 55.0 billion, so almost the entire top line still comes from ads and not from futuristic hardware bets.

Furthermore, family daily active people reached about 3.56 billion in March 2026, up 4 percent versus last year, even though there was a slight dip versus the previous quarter due to outages in Iran and restrictions in Russia. So engagement is not collapsing; it is nudged around by geopolitics and network disruptions, not by users leaving en masse. In fact, when you combine more users with more ad impressions and higher ad pricing, you get a powerful compounding effect on revenue.

Because the operating margin stayed at about 41 percent despite a very heavy research and development budget, the underlying digital ad franchise still looks highly profitable. Therefore, from a fundamental point of view, the dip is not about a broken advertising model; it is mainly about how much cash gets ploughed back into AI and hardware over the next few years.

Price action: a sharp swing in meta stock

Before this earnings release, the stock had already rallied strongly, gaining roughly 20 percent over the previous month as investors chased AI‑linked winners and big‑tech names. So expectations were high, and short‑term traders were positioned for a perfect report with no negative surprises on spending.

However, once the higher capex forecast hit the tape, the narrative flipped from “AI winner” to “AI cost monster,” and the stock sold off in after‑hours trading and pre‑market sessions. On many historical occasions, this stock has gapped down by 10–20 percent after big announcements about spending or regulatory risk, and this move fits right into that patt

Valuation snapshot: where does meta trade now?

Next, it is useful to look at valuation. Various data providers show that the current price‑to‑earnings multiple, on a trailing basis, sits in the mid‑20s range, which is above the depressed levels of late 2022 but still below the peak multiples during the 2021 mania. Importantly, earnings per share have grown sharply over the last few years, while the P/E ratio has not expanded at the same pace, which means a good portion of the recent share price move has actually been backed by real profit growth.

Because net income jumped about 61 percent year on year this quarter and diluted EPS rose roughly 62 percent, the stock is not purely running on hype. Even at a mid‑20s multiple, a business with this kind of growth, cash generation and margin profile can still be reasonably valued when compared with many slower‑growing consumer names. However, if future years see heavy capex and a slower profit ramp, the multiple can compress again, which is exactly what short‑term traders are worried about today.

Investment cycle: heavy spending, harsh reactions

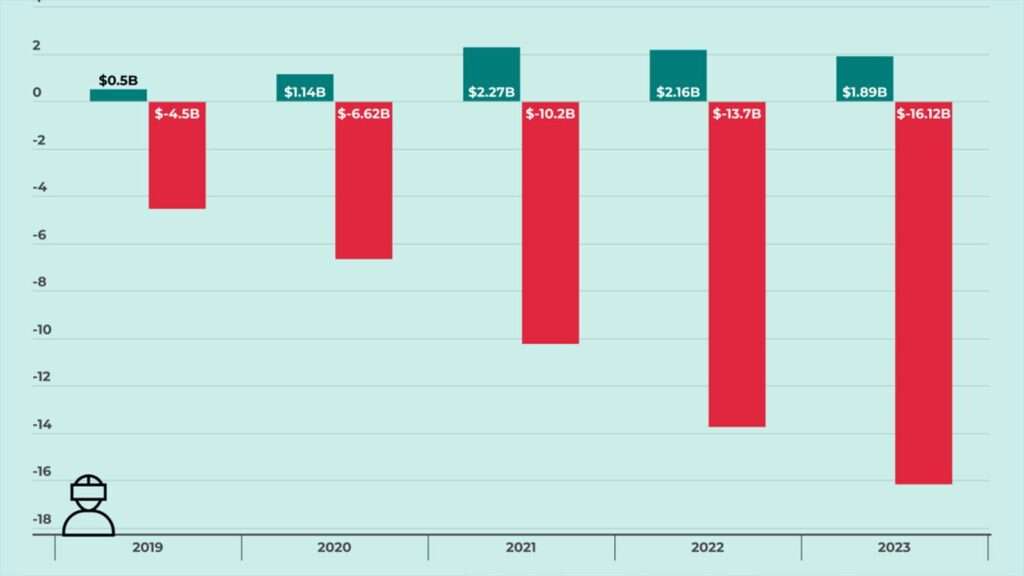

Now comes the controversial part. Management has clearly said that 2026 capex will be in the 125–145 billion range as it builds AI supercomputing infrastructure and next‑generation data centers. Reality Labs, the segment that houses virtual and augmented‑reality devices along with related software, generated only about 0.4 billion in revenue this quarter but burned roughly 4.0 billion at the operating level.

Over the past few years, Reality Labs has racked up tens of billions in cumulative operating losses, and external trackers estimate that total losses have crossed 70 billion when you add up multiple years. So markets have a long memory; whenever management doubles down on this investment cycle, investors instantly remember how painful the last one felt. Yet, these same investment waves in infrastructure and features also tended to precede strong revenue and profit growth once the platforms matured.

Therefore, what we are seeing now is not new. When the firm shifted to mobile, to stories, and to short‑form video, there were periods of rising costs, falling margins, grim headlines and sharp stock corrections. But later, as the monetisation engine caught up, those who had held through the volatility were often rewarded, while those who sold on fear ended up re‑entering at higher levels.

Data and fundamentals: can this be sustained?

From a balance sheet angle, the company still sits on a very large cash and investments pile of roughly 81 billion, with total assets around 395 billion and equity of about 244 billion. Cash flow from operations for the quarter was over 32 billion, while free cash flow, after capex and lease payments, came in at around 12.4 billion. So the business can fund a lot of its AI and hardware push from internal cash generation instead of relying entirely on debt or equity dilution.

Moreover, headcount is growing very slowly, just about 1 percent year on year, which suggests that management is trying to stay disciplined on payroll even while it pours money into chips and data centers. The family of apps segment produced about 26.9 billion in operating income, which easily covered the 4.0 billion Reality Labs loss and still left a thick profit cushion. Therefore, as long as the advertising franchise keeps compounding, the investment budget has a strong engine behind it.

However, there are real risks. Legal and regulatory headwinds, especially around youth safety and data privacy, are explicitly flagged in the company’s own outlook commentary, and there are upcoming trials that could result in material financial hits. Additionally, if macro conditions worsen and ad budgets slow, even a strong platform can face growth headwinds, which would make heavy capex plans look more aggressive in hindsight.

Chart reading: where might long‑term investors focus?

From a chart perspective, this latest drop comes after a fast, almost vertical rally, which often creates weak hands in the shareholder base. In many past cycles, the stock has formed new base ranges after such gaps, consolidating sideways while fundamentals catch up, before attempting fresh breakouts.

Technical traders might watch zones around prior breakout levels or moving averages as potential “demand pockets,” while long‑term investors may simply use a systematic plan, such as staggered buying over several months rather than a single big entry. Because volatility is high, position sizing becomes critical; even a great business can hurt if you over‑concentrate near short‑term tops.

Interestingly, this is similar to how bloggers and YouTubers look for low‑competition keywords instead of chasing the most crowded phrases: investors can look for quality companies temporarily out of favour rather than chasing parabolic moves. Just as “why is this stock falling after strong earnings” can be a long‑tail query with high intent, a sharp but temporary drawdown in a still‑profitable business can be a place to study deeper rather than to panic.

Personal targets, upside and realism

You mentioned personal upside targets of around 850 by early 2027 and about 1,100 in two to three years. Those levels imply meaningful compounding from today’s price, and they assume that the ad engine keeps growing, AI investments translate into higher monetisation and Reality Labs losses stay manageable. They also assume that the market continues to reward the stock with at least a healthy mid‑20s earnings multiple, if not higher.

However, markets rarely move in straight lines. Along the way, there can be macro shocks, more regulatory news, or even product missteps that trigger fresh 20–30 percent drawdowns. Therefore, it helps to treat these target prices as flexible scenarios, not as guaranteed destinations. In other words, your thesis can be right but your timeline can still be wrong, which is why risk management and patience are as important as picking the right business.

Risk, volatility and a very clear disclaimer

Now, it is very important to underline this part. Everything in this post is only analysis and education based on public numbers and market data. It is not a suggestion to buy, to sell or to hold any security, including this one.

Stock markets are risky and can change very quickly. Prices can move due to factors that no model or blog can predict in advance. You should always do your own due diligence, read official filings, understand your risk tolerance and, if needed, consult a registered investment advisor before acting on any idea.

If you decide to use this dip as an opportunity, that is your personal call and responsibility. If you choose to wait, reduce exposure or avoid the name entirely, that is also completely valid. The real edge often comes from having a process that fits your own goals, not from copying anyone’s trades.

How a calm long‑term investor might think about this dip

Putting it all together, the picture looks like this. The core advertising business is strong, growing in the low‑30s percent range with world‑class margins and very high cash generation. The balance sheet is solid, and the company is willing to reinvest aggressively in AI infrastructure and hardware, even if that hurts short‑term reported profits.

The market, meanwhile, is punishing that reinvestment with a sharp price drop after a big prior run‑up. Historically, such phases of heavy spending coupled with noisy headlines have given long‑term investors some of their best entry points, provided they were ready for volatility and used sensible position sizing. Therefore, this dip can be a moment to sharpen your thesis, revisit your numbers and decide whether this alignment of strong fundamentals and weak sentiment fits your own strategy.

But again, this is a framework, not a forecast. What you finally do with it should come from your own research, your own constraints and your own comfort with risk.

👉 You Might also find this post insightful – https://bosslevelfinance.com/meta-2025-simple-truths-about-cash-and-ai

Sources (for further reading)

???? You Might Also Like: Should You Invest in AI Chip Leader Right Now?

Pingback: Should You Invest in AI Chip Leader Right Now? -