Understanding NVIDIA’s Dominance in AI Chip Market

Let me tell you something exciting. NVIDIA has become the backbone of artificial intelligence. Moreover, the company now controls roughly 80-85% of the AI chip market. That’s massive dominance, friends.

But here’s the thing. Can this tech giant maintain its incredible momentum through 2026? Furthermore, is this the right time for retail investors to consider this stock? Let’s dive deep into the numbers and find out.

NVIDIA Revenue Growth: Breaking Down the Numbers

First, let’s talk about revenue. NVIDIA reported stunning Q4 fiscal 2025 results. Therefore, the numbers speak volumes about their market position.

The company generated $39.3 billion in Q4 revenue. Additionally, this marks a 78% jump compared to last year. Even more impressive? Full-year revenue hit $130.5 billion. That’s a whopping 114% increase year-over-year.

Now, here’s where it gets interesting. The Data Center segment alone brought in $115.2 billion for fiscal 2025. Consequently, this represents a 142% surge from the previous year.

Data Center Business: The Real Money Maker

Let me break this down simply. Data centers are NVIDIA’s golden goose right now. In fact, Q4 Data Center revenue reached $35.6 billion. That’s up 93% year-over-year.

Meanwhile, major cloud providers are scrambling for NVIDIA chips. Companies like Microsoft Azure, Google Cloud, and Amazon AWS cannot get enough. Therefore, the demand seems unstoppable.

Furthermore, NVIDIA announced a mind-blowing $500 billion order backlog. This includes both Blackwell and upcoming Rubin chips. Basically, this guarantees strong revenue through 2027.

However, here’s something to consider. Goldman Sachs predicts NVIDIA could generate over $300 billion in AI data center revenue for 2026 alone. That’s phenomenal growth, my friends.

NVIDIA Stock Price Analysis: Where Are We Heading?

Currently, NVIDIA stock trades around $185 per share. But analysts see significant upside potential. In fact, Goldman Sachs maintains a $250 price target. This suggests a potential 35% gain from current levels.

Moreover, the average analyst price target sits around $260. That represents over 40% upside potential. Pretty compelling, right?

Yet, we must stay realistic. The stock has already surged 1,252% over the past five years. Therefore, some consolidation seems natural after such explosive gains.

Additionally, recent market volatility has impacted tech stocks. NVIDIA isn’t immune to broader market concerns. Thus, short-term fluctuations are expected.

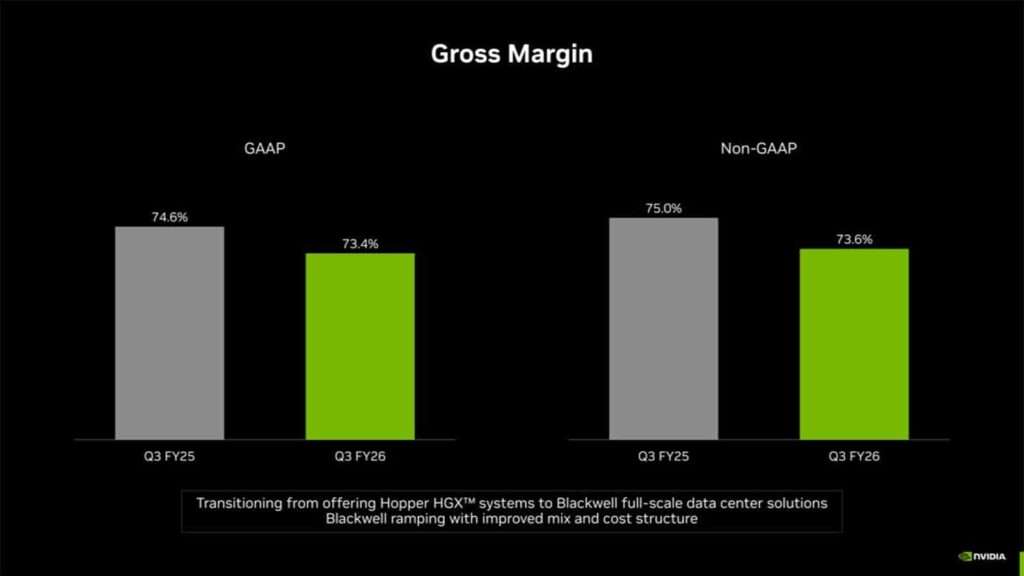

Fundamental Analysis: Is NVIDIA Stock Overvalued or Undervalued?

Let’s examine the fundamentals carefully. NVIDIA maintains exceptional profit margins. Specifically, the gross margin stands at 73.5% for Q4. That’s incredibly healthy for a chip manufacturer.

Furthermore, earnings per share reached $2.94 for fiscal 2025. This represents a 147% increase year-over-year. Clearly, profitability keeps accelerating.

However, valuation matters too. NVIDIA’s market cap recently touched $5 trillion. That makes it the world’s most valuable company occasionally. But is this justified?

Here’s my perspective. The company dominates a rapidly growing market. AI spending continues expanding globally. Therefore, premium valuation seems somewhat justified.

Nevertheless, competition is heating up. AMD currently holds 7% market share and growing. Additionally, companies like Intel and Qualcomm are launching competitive chips. Thus, NVIDIA must innovate constantly.

Gaming and Professional Visualization Segments Performance

Now, let’s discuss other business segments. Gaming revenue was $2.5 billion in Q4. Unfortunately, this dropped 11% year-over-year. Why? Limited availability of Blackwell and Ada GPUs affected sales.

However, don’t worry too much. Full-year gaming revenue still grew 9% to $11.4 billion. Moreover, the new GeForce RTX 50 Series just launched. This should boost gaming revenue soon.

Meanwhile, Professional Visualization brought in $1.9 billion annually. That’s up 21% year-over-year. Consequently, this segment shows steady growth potential.

Additionally, the Automotive segment generated $1.7 billion. This jumped 55% compared to last year. Clearly, NVIDIA’s push into self-driving technology pays off.

NVIDIA’s Competitive Advantages: Why They Stay Ahead

Here’s what makes NVIDIA special. The company built an incredible software ecosystem called CUDA. Basically, millions of developers already use this platform. Therefore, switching to competitors becomes extremely difficult.

Moreover, NVIDIA invests heavily in research and development. They consistently launch next-generation chips. For instance, the Rubin chip launches in late 2026. This promises even better performance than Blackwell.

Furthermore, strategic partnerships strengthen their position. The $500 billion Stargate Project partnership shows confidence. Additionally, collaborations with OpenAI and major cloud providers create sticky relationships.

However, staying ahead requires constant innovation. Competition never sleeps in technology. Thus, NVIDIA must maintain aggressive R&D spending.

Risk Factors: What Could Go Wrong?

Let me be honest about risks. Several factors could impact NVIDIA negatively. First, excessive dependence on data center revenue creates vulnerability. Currently, this segment represents nearly 90% of revenue. Therefore, any slowdown would hurt significantly.

Second, geopolitical tensions pose risks. Trade restrictions with China could limit market access. Additionally, export controls on advanced chips create complications.

Third, competition intensifies daily. AMD aggressively pursues market share. Moreover, custom AI chips from Google and Amazon could reduce dependency on NVIDIA.

Fourth, valuation concerns remain valid. At current prices, the stock trades at premium multiples. Thus, any earnings disappointment might trigger sharp corrections.

Finally, manufacturing challenges could arise. Chip production requires complex supply chains. Therefore, any disruption impacts product availability.

Upcoming Catalysts: What to Watch

Several catalysts could drive the stock higher. First, Q4 fiscal 2026 earnings release on February 25th. Analysts expect revenues around $67 billion. Beating expectations would boost sentiment significantly.

Second, Rubin chip launch in late 2026. This next-generation GPU promises substantial performance improvements. Therefore, successful rollout could accelerate growth.

Third, expanding AI adoption globally. More companies implement AI solutions daily. Consequently, chip demand should remain strong.

Fourth, new market opportunities emerge. Autonomous vehicles and robotics represent huge potential. Moreover, edge AI applications are growing rapidly.

Finally, potential stock buybacks and dividends. NVIDIA returned $8.1 billion to shareholders in Q4. Thus, continued capital returns support stock prices.

NVIDIA’s Financial Health: Margins and Profitability

Let’s examine financial strength closely. NVIDIA maintains exceptional profitability metrics. Operating margins exceed 60% consistently. That’s remarkable efficiency, friends.

Additionally, the company generates massive free cash flow. This funds aggressive R&D investment. Moreover, it supports shareholder returns through buybacks and dividends.

Furthermore, the balance sheet remains fortress-strong. NVIDIA carries minimal debt relative to assets. Therefore, financial flexibility stays excellent.

However, operating expenses are rising. They jumped 45% year-over-year in Q4. Consequently, margin expansion becomes challenging. Nevertheless, absolute profit dollars keep growing impressively.

Long-Term Investment Perspective on NVIDIA Stock

Here’s my honest assessment for long-term investors. NVIDIA operates in a massive growth market. AI adoption is still early innings. Therefore, the runway extends many years ahead.

Moreover, the company demonstrates consistent execution. Management delivers on promises quarter after quarter. Additionally, technological leadership remains unquestioned currently.

However, buying at current levels requires conviction. The stock isn’t cheap by traditional metrics. Thus, investors need belief in sustained growth.

Furthermore, volatility should be expected. Tech stocks fluctuate significantly short-term. Therefore, strong hands and patience become essential.

My suggestion? Consider dollar-cost averaging instead of lump-sum investing. This reduces timing risk significantly. Moreover, it smooths out volatility impact.

Comparing NVIDIA with Competitors in AI Chip Space

Let’s briefly compare NVIDIA with rivals. AMD shows promise but lags significantly. Their market share remains under 10% currently. However, they’re investing aggressively to catch up.

Meanwhile, Intel struggles to regain relevance. Their chips haven’t matched NVIDIA’s performance yet. Therefore, they’re playing catch-up in AI.

Additionally, custom chips from hyperscalers pose threats. Google’s TPUs and Amazon’s Trainium chips serve their ecosystems. Thus, they reduce NVIDIA dependency somewhat.

However, NVIDIA maintains clear advantages. CUDA ecosystem creates powerful moat. Moreover, performance leadership continues with each generation. Therefore, displacing them seems extremely difficult.

Technical Analysis: Chart Patterns and Price Levels

From a technical perspective, NVIDIA shows interesting patterns. The stock recently bounced from support around $170. This suggests buyers stepped in aggressively.

Moreover, resistance exists around $210-220 zone. Breaking above this level could trigger momentum. Therefore, watch these levels closely.

Additionally, the 50-day moving average provides support. Currently, this sits near $184. Consequently, holding above this remains bullish.

However, the 200-day moving average at $170 offers stronger support. A break below might signal deeper correction. Thus, this becomes critical level to monitor.

Furthermore, RSI indicators show neutral territory. This suggests neither overbought nor oversold conditions. Therefore, the stock could move either direction near-term.

Final Thoughts: Is NVIDIA Stock Worth Buying in 2026?

So, what’s the verdict? NVIDIA clearly dominates AI infrastructure market. Moreover, fundamentals remain impressively strong. Revenue growth, profitability, and market position all shine brightly.

However, valuation demands premium prices. The stock isn’t bargain-priced currently. Therefore, investors need conviction about AI’s long-term growth.

Additionally, competition will intensify gradually. NVIDIA cannot rest comfortably. Thus, execution becomes critical for maintaining leadership.

My perspective? NVIDIA represents a quality long-term holding. But timing matters for entry points. Consider accumulating on weakness rather than chasing rallies.

Furthermore, position sizing remains crucial. Don’t bet everything on single stock. Proper diversification protects against unexpected risks.

Finally, remember this analysis doesn’t constitute investment advice. Markets remain unpredictable always. Do thorough research before making decisions. Consult qualified financial advisors. Never invest money you cannot afford losing.

The AI revolution continues unfolding. NVIDIA stands positioned incredibly well. However, smart investing requires patience, discipline, and realistic expectations. Stay informed, stay rational, and invest wisely.

👉 You Might also find this post insightful – https://bosslevelfinance.com/stx-opportunity-seagates-storage-edge-in-the-ai-boom

Disclaimer: This analysis is for educational purposes only. We do not encourage you to buy, sell, or hold any stocks. Stock markets are subject to risks and volatility. Always do your own due diligence before making any investment decisions. Consult a financial advisor for personalized advice.

Source Links

- https://pintu.co.id/en/news/254985-nvidia-nvda-stock-analysis-2026-buy-sell-hold/amp

- https://finance.yahoo.com/news/nvidia-corp-nvda-q4-2025-072422920.html

- https://www.ainvest.com/news/nvidia-path-dominance-2026-ai-momentum-sustain-record-growth-2512/

- https://finance.yahoo.com/news/goldman-sachs-revamps-nvidia-stock-184524432.html

- https://www.reddit.com/r/nvidia/comments/1iyz82e/nvidia_fiscal_q4_2025_financial_result/

- https://www.fool.com/investing/2025/12/18/which-ai-chip-stock-is-the-better-buy-for-2026-nvi/

- https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-fourth-quarter-and-fiscal-2025

- https://www.ainvest.com/news/nvidia-2026-growth-catalysts-backlog-margins-market-positioning-2512/

- https://finance.yahoo.com/news/nvidias-85-gpu-market-share-210500376.html

- https://www.nasdaq.com/articles/prediction-nvidia-stock-going-soar-after-feb-25

- https://www.cnn.com/2026/02/07/business/nvidia-trillion-valuation-ai-chips-vis