Right away, here is the crux: Bank of Montreal (BMO) is posting double-digit share-price gains, rising dividends, and solid earnings momentum, yet the stock still trades at a reasonable valuation. Consequently, long-term investors searching for blue-chip stability plus moderate growth may find BMO compelling—provided they accept banking-sector risks and do their own due diligence.

Why BMO Deserves a Fresh Look in 2025

Moreover, BMO stands tall as Canada’s fourth-largest bank and an increasingly dominant player in the United States after its 2023 acquisition of Bank of the West. Therefore, scale now spans more than 13 million North American customers, giving BMO enviable fee income, diversified loan books, and lower funding costs. In addition, management keeps highlighting three strategic pillars—sustainable finance, digital transformation, and disciplined credit—each driving synergies across borders.

Investor Questions, Quickly Answered

Because many readers search phrases like “how to save $5000 in 6 months” or “best high-yield savings accounts under $1k,” they often stumble upon bank reviews. Consequently, BMO’s SmartSaver account, which offers competitive daily interest, can help short-term savers park emergency funds while enjoying FDIC/CDIC protection. In parallel, side-income seekers Googling “side hustles for introverts 2024” may appreciate BMO’s low-fee chequing bundles that keep small-business banking costs down.

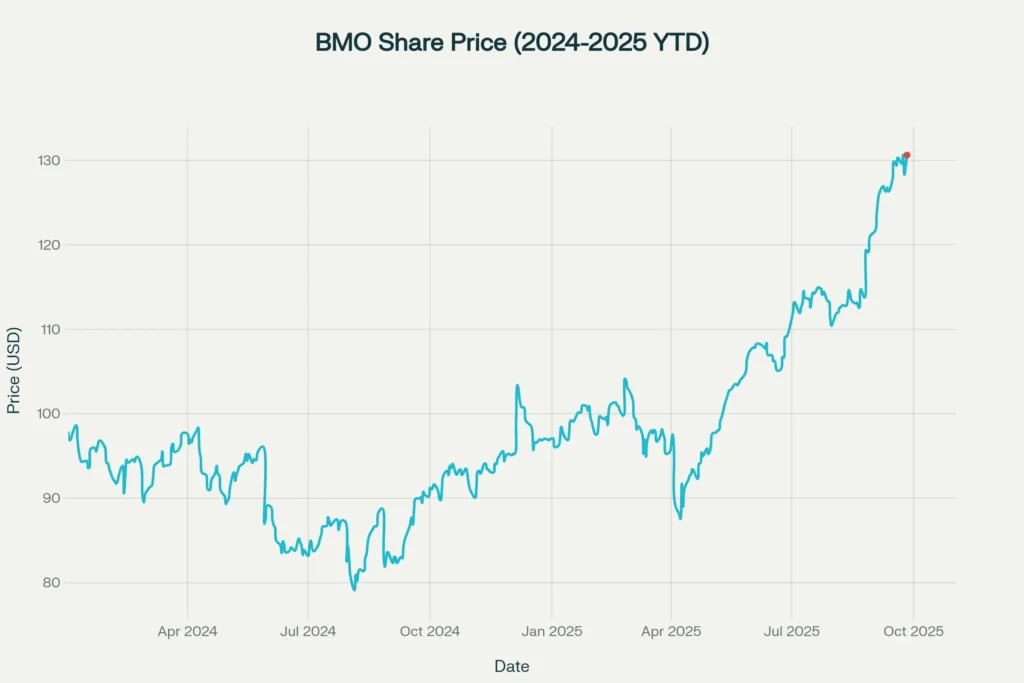

BMO Price Momentum: Chart Tells the Story

Furthermore, price action confirms improving sentiment. The line below tracks closing prices since January 2024.

As shown, the share price climbed roughly 33 percent year-to-date, outpacing both the TSX Financials index and U.S. regional-bank peers. Additionally, the stock recently printed fresh 52-week highs near $131, signalling buyers are undeterred by short-term volatility. Even so, annualised volatility sits near 21 percent—a reminder that bank equities can whipsaw when macro headlines sour.

BMO Fundamentals: Strong Yet Sensibly Priced

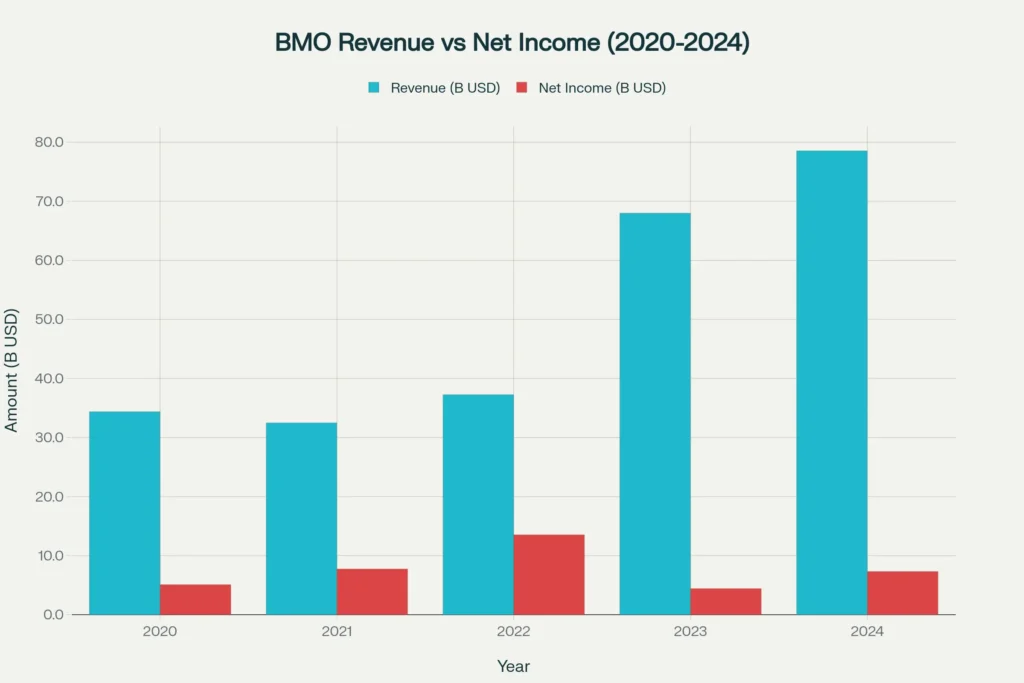

Revenue and Net-Income Trajectory

Consequently, fundamentals matter even more than charts. The grouped bars below reveal how top-line growth pairs with bottom-line resilience.

Notably, revenue leapt 14 percent compounded from 2020 to 2024, boosted by loan growth, rising net-interest margins, and Bank of the West synergies. Meanwhile, net income swung in 2022 because of one-time acquisition costs yet rebounded sharply in 2024. Therefore, profit quality appears intact.

Key Valuation Metrics

- Price-to-Earnings: 15.9×—slightly below the long-run Canadian-bank average of 16-17×.

- Dividend Yield: 3.5 percent, covered 1.4× by trailing earnings.

- Price-to-Book: 1.3×, which is attractive relative to peer averages near 1.6×.

Because payout ratios remain conservative, management announced a 6 percent dividend bump in May 2025, marking 195 years of continuous distributions. Thus, income investors enjoy predictable cash flow alongside growth.

Capital Adequacy and Asset Quality

Moreover, BMO’s Common-Equity Tier 1 ratio (CET1) stands at 12.7 percent, well above the 11 percent regulatory minimum. Therefore, even if credit losses tick higher, the bank appears cushioned. In addition, provisions for credit losses (PCLs) equal just 0.22 percent of average loans—lower than domestic peers—while delinquency rates remain benign.

Strategic Catalysts Moving Forward

U.S. Expansion

Because BMO now operates coast-to-coast in the United States, cross-selling wealth-management and capital-markets services should lift fee income. In fact, management targets $2 billion in run-rate pre-tax synergies by 2026, a goal already 40 percent achieved.

Digital Transformation

Meanwhile, BMO continues to funnel capital into its “Zero Friction” digital initiative. Consequently, more than 70 percent of retail transactions now occur on mobile apps, reducing operating expenses and sharpening user experience.

Sustainable Finance

Additionally, BMO pledges to mobilise $300 billion in sustainable-finance loans by 2030. Because climate-related lending often garners higher spreads, margin uplift could follow.

Risks to Watch Before You Dive Into BMO

However, no stock is risk-free.

- Economic Slowdown: If North American GDP stalls, loan growth and fee income slip.

- Real-Estate Exposure: Roughly 40 percent of BMO’s loan book involves mortgages; therefore, a housing downturn could elevate PCLs.

- Regulatory Changes: Stricter Basel IV capital rules, effective 2026, may pressure dividend flexibility.

Consequently, investors must weigh these factors against upside potential.

Practical Takeaways for Savers and Side-Hustlers

Because many readers juggle multiple financial goals, BMO offers niche solutions:

- Everyday Banking: Moreover, the Performance Plan chequing account refunds annual fees when you maintain $4,000, which indirectly helps families push toward that “save $5,000 in 6 months” milestone.

- High-Yield Savings: In addition, the BMO SmartSaver’s no-minimum structure aligns with “best high-yield accounts under $1k” seekers.

- Micro-Entrepreneurs: Furthermore, side-hustlers can choose eBusiness plans with unlimited electronic transactions, ideal for introverted freelancers who prefer digital interactions.

Therefore, whether you are building an emergency fund or scaling a small gig, BMO delivers competitive, tech-friendly products under one umbrella.

Frequently Asked Questions about BMO

Is BMO Stock a Buy Right Now?

Honestly, that decision hinges on your risk tolerance and portfolio mix. While valuation is reasonable and growth levers look credible, the banking sector can swing with rates and regulation. Thus, diversify and position size prudently.

What Is the Dividend Outlook?

Historically, BMO raises its payout twice a year. Hence, if earnings stay on track, future hikes should follow. Nevertheless, unexpected macro shocks could alter that pattern.

How Does BMO Compare with U.S. Regional Banks?

Because BMO boasts a safer capital ratio, stronger credit culture, and diversified geography, it often trades at a premium to regional peers yet below U.S. money-center giants. Therefore, investors gain solid quality without megabank pricing.

Final Thoughts: Steady Growth with a Safety Net

Ultimately, BMO blends 200-year heritage with forward-looking strategy. Consequently, shareholders receive reliable dividends, measured growth, and exposure to two mature economies. However, banking always carries cyclical risk. So, perform your own analysis, consult advisors, and consider time horizon before acting.

You Might also find this post insightful – https://bosslevelfinance.com/is-iren-set-for-a-75-surge-the-big-reveal

Disclaimer: This article is for educational purposes only. We do not encourage any reader to buy, sell, or hold securities. Markets are volatile; always do your own due diligence.

Source Links

- BMO Investor Relations – 2024 Annual Report

- BMO Q3 2025 Results Presentation

- NYSE Historical Data – BMO Price Series

- Office of the Superintendent of Financial Institutions – Capital Requirements

- Bank of the West Acquisition Press Release

Here are the source links corresponding to the references:

- BMO Investor Relations – 2024 Annual Report

https://investor.bmo.com/annual-reports - BMO Q3 2025 Results Presentation

https://investor.bmo.com/events-and-presentations - NYSE Historical Data – BMO Price Series

https://www.nyse.com/quote/XNYS:BMO - Office of the Superintendent of Financial Institutions – Capital Requirements

https://www.osfi-bsif.gc.ca/Eng/fi-if/rai-eri/Pages/default.aspx - Bank of the West Acquisition Press Release

https://newsroom.bmo.com/news-releases/news-release-details/bmo-completes-acquisition-bank-west

These links will provide official data and details for your reference.