Qualcomm’s (QCOM) core story is straightforward: revenue and earnings are rising again, diversification beyond smartphones is working, and automotive plus edge-AI are becoming real growth engines even as competitive and policy risks stay in view. Therefore, investors tracking semiconductors should note year-over-year revenue growth, expanding non-GAAP EPS, and segment gains in chips (QCT) and licensing (QTL), while staying mindful of Apple modem insourcing, Android competition, and tariff uncertainty. Moreover, consensus targets still imply upside from current levels, yet volatility and cyclical dynamics demand caution and robust risk management. Finally, this is analysis, not advice, and markets can change quickly—please do your own due diligence.

QCOM Snapshot: What Changed And Why It Matters

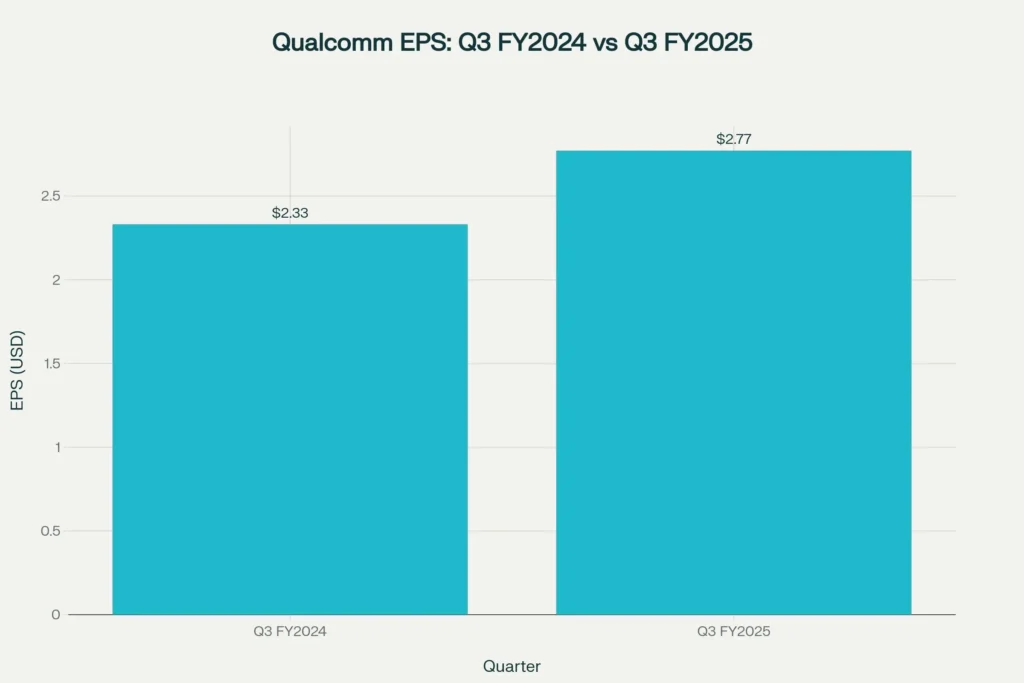

First, Qualcomm delivered double-digit year-over-year revenue growth in recent quarters, with Q3 FY2025 revenue near $10.37 billion and non-GAAP EPS of $2.77, reflecting broad-based execution beyond core smartphones. Additionally, the chip business (QCT) posted gains as premium Android and AI features lifted average selling prices, even as volumes remain uneven across tiers. Moreover, automotive revenue surged on design wins and pipeline momentum, signaling a credible runway as vehicles become software-defined computers on wheels. However, Apple’s move to in-house modems, tariff noise, and intense competition from MediaTek in the mid-range handset market remain key overhangs to monitor.

Fundamentals: Revenue, Margins, And Diversification

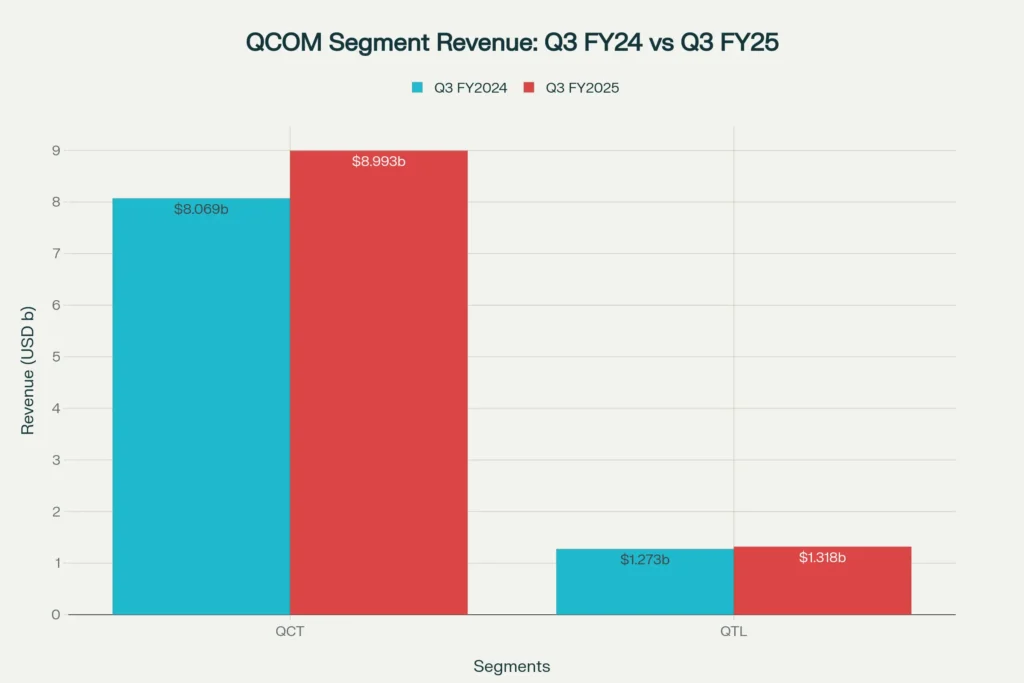

To begin, Qualcomm’s Q3 FY2024 print showed revenue of $9.39 billion with QCT up 12% year over year and QTL up 3% year over year, while non-GAAP EPS reached $2.33 on improving mix and disciplined opex. Furthermore, by Q3 FY2025, revenue rose roughly 10% year over year and non-GAAP EPS improved to $2.77, indicating operational leverage as automotive and IoT contributions scale. And importantly, licensing remains a high-margin anchor, while chips drive top-line growth through premium Android, PCs with Snapdragon X, and connected devices at the edge. Consequently, diversification reduces dependence on any single end market, although the handset cycle still influences quarterly swings.

QCOM And The AI Wave: Where The Edge Meets The Cloud

Because AI is moving on-device, Qualcomm positions its Snapdragon platforms as engines for personal AI—enabling image generation, speech tasks, and multimodal features without the cloud round-trip. Moreover, this edge-AI push complements industry growth in data centers, HBM memory, and accelerators, where ecosystem capacity and packaging innovations are transforming the performance-per-watt frontier. And since latency, privacy, and cost matter at scale, on-device intelligence can expand premium tiers and drive refreshed cycles across phones, PCs, XR glasses, and embedded IoT endpoints. Therefore, as AI PCs and mixed-reality devices proliferate, Qualcomm’s design wins and developer traction become critical leading indicators for durable monetization.

Segments To Watch: Handsets, Automotive, And IoT

Handsets still dominate near-term revenue, and although unit growth is modest, the premium tier expands as flagship features and AI lift value per device. Meanwhile, automotive semiconductors are compounding from a small base, with Qualcomm citing strong design-win momentum across digital cockpit, connectivity, and ADAS compute. Additionally, IoT is stabilizing with a healthier mix in consumer and enterprise devices, including wearables, XR, and edge compute products that benefit from AI workloads. Thus, a multi-engine model is taking shape: smartphones fund R&D, automotive adds long-cycle visibility, and IoT provides breadth across fast-evolving edge categories.

Technical And Chart Perspective: Levels And Context

From a market lens, Qualcomm’s shares experienced notable swings post-2024 highs, reflecting both cyclical semiconductor dynamics and company-specific news flow on customers and policy risk. Moreover, analysts’ price targets cluster around the high $170s to low $180s on average, with upside scenarios tied to AI adoption curves and automotive execution. And while near-term volatility remains, improving EPS trends and segment breadth provide a constructive medium-term setup if macro headwinds and policy risks ease. Therefore, traders often watch the prior breakout zones and moving averages for risk framing, while long-term investors focus on multi-year earnings power across end markets.

Valuation: Is The Multiple Reasonable For The Growth Mix

Because consensus projects continued revenue and EPS expansion, the current valuation has toggled between mid-teens and high-teens P/E depending on macro and handset sentiment. Furthermore, as automotive and AI PCs scale, some investors expect a quality re-rating if margins sustain and if licensing remains resilient despite legal and competitive noise. And since semiconductors are cyclical, patient capital typically seeks entries during dislocations tied to tariffs, handset pauses, or supply chain headlines. Consequently, valuation depends less on one quarter and more on the credibility of a three-year road map spanning premium Android, auto, IoT, and on-device AI PCs.

qcom Risk Checklist: What Could Go Wrong

Obviously, Apple modem insourcing is a headwind to long-run modem revenue with uncertain timing and magnitude across product cycles. Additionally, tariff and export-policy shifts can alter demand timing, mix, and customer behavior, with episodic volatility around earnings windows. Moreover, MediaTek competition in the mid-range smartphone tier pressures share and pricing, while Android cycles can drive unpredictable inventory corrections. Finally, execution risk in automotive and AI PCs remains, since long design cycles, platform transitions, and ecosystem dependencies can delay revenue realization.

Industry Tailwinds: Why The Setup Still Looks Constructive

Crucially, the semiconductor industry’s secular drivers—AI, cloud, automotive, edge compute—point to sustained growth through the decade even amid cyclical pauses. Furthermore, capex, packaging innovation, and foundry advances at leading nodes support performance gains required by AI workloads and software-defined vehicles. And because Qualcomm is fabless with a deep IP portfolio, it can channel R&D into differentiated system solutions for low-power compute at the edge. Therefore, if management continues to execute on design wins, software integration, and partner ecosystems, operating leverage can improve through the next device cycle.

Actionable Takeaways: Simple Rules For A Complex Cycle

First, focus on segments: watch automotive revenue trajectory and AI PC adoption as validation for diversification beyond handsets. Next, track margins and EPS trends as proxies for pricing, mix, and cost control through the cycle. Then, monitor policy headlines and Apple modem milestones to manage expectations on medium-term chip revenue risk. Finally, align entries and sizing with your risk tolerance, because cyclical swings can be sharp even in strong secular stories.

Clear Disclaimer And Reader Guidance

This article is solely analysis and education, and it is not investment advice or a recommendation to buy, sell, or hold any security, including Qualcomm. Markets are volatile and subject to rapid change, and past performance is not indicative of future results. You should do your own research and consult a qualified advisor before making financial decisions that involve risk of loss. Please use this discussion as one input among many in your independent due diligence process.

Conclusion: A Pragmatic, Easy-To-Use Framework

In sum, Qualcomm’s improving revenue, rising EPS, and healthier segment mix suggest a constructive multi-year path if edge-AI, auto, and IoT deliver as planned. Moreover, while competition and policy risk can rattle shares, the secular setup in semiconductors remains favorable with AI and automotive pulling the sector forward. Therefore, a balanced approach—watching segment KPIs, monitoring margins, and respecting volatility—offers a simple, repeatable way to track progress without getting lost in noise. And as always, keep your process disciplined, keep your time horizon clear, and keep learning through each cycle to improve outcomes over time.

👉 You Might also find this post insightful – https://bosslevelfinance.com/how-jmp-is-winning-in-the-financial-sector-now

👉 Create a Vested Account today to start investing in US Stocks – https://refer.vestedfinance.com/RUKU88007

- https://stockanalysis.com/stocks/qcom/

- https://s204.q4cdn.com/645488518/files/doc_financials/2024/q3/FY2024-3rd-Quarter-Earnings-Release.pdf

- https://www.cnbc.com/2024/07/31/qualcomm-qcom-earnings-report-q3-2024.html

- https://simplywall.st/stocks/us/semiconductors/nasdaq-qcom/qualcomm

- https://s204.q4cdn.com/645488518/files/doc_financials/2025/q3/FY2025-3rd-Quarter-Earnings-Release.pdf

- https://www.marketbeat.com/stocks/NASDAQ/QCOM/forecast/

- https://finance.yahoo.com/news/qualcomm-forecasts-revenue-above-estimates-200230429.html

- https://futurumgroup.com/insights/qualcomm-fyq3-2024-earnings/

- https://www.nasdaq.com/articles/qualcomm-qcom-q3-revenue-jumps-10

- https://www.investing.com/news/stock-market-news/qualcomm-forecasts-revenue-above-estimates-betting-on-ai-use-to-drive-chip-demand-4161021

- https://www.pwc.com/gx/en/industries/technology/state-of-the-semicon-industry.html

- https://telecom.economictimes.indiatimes.com/news/devices/qualcomm-forecasts-trump-tariffs-will-dent-revenue-shares-fall-6/120781861

- https://www.mordorintelligence.com/industry-reports/semiconductor-industry-landscape

- https://www.startus-insights.com/innovators-guide/semiconductors-trends-innovation/

- https://www.fxleaders.com/news/2025/07/30/qualcomm-qcom-surpasses-revenue-forecasts-rides-ai-chip-demand-wave/

- https://in.tradingview.com/symbols/NASDAQ-QCOM/

- https://www.marketwatch.com/investing/stock/qcom

- https://www.google.com/finance/beta/quote/QCOM:NASDAQ

- https://in.tradingview.com/symbols/NASDAQ-QCOM/forecast/

- https://www.marketwatch.com/investing/stock/qcom/analystestimates

- https://www.valueresearchonline.com/stocks/45582/qualcomm-incorporated-qcom/

- https://www.infosys.com/iki/research/semiconductor-industry-outlook2025.html

- https://finance.yahoo.com/quote/QCOM/history/

- https://finance.yahoo.com/quote/QCOM/

- https://investor.qualcomm.com/stock-info/quote/default.aspx

- https://simplywall.st/stocks/us/semiconductors/nasdaq-qcom/qualcomm/news/evaluating-qualcomm-qcom-after-recent-gains-is-the-stock-und

- https://www.fortunebusinessinsights.com/semiconductor-market-102365

- https://finance.yahoo.com/news/qualcomm-nasdaq-qcom-beats-q3-212824934.html

- https://www.expertmarketresearch.com/reports/semiconductor-market

- https://www.cnn.com/markets/stocks/QCOM

- https://stockstory.org/us/stocks/nasdaq/qcom

- https://coincodex.com/stock/QCOM/price-prediction/

- https://www.quiverquant.com/news/$QCOM+stock+is+down+7%25+today.+Here’s+what+we+see+in+our+data.

- https://www.capgemini.com/us-en/insights/expert-perspectives/7-major-trends-shaping-the-future-of-the-semiconductor-industry/

- https://www.investopedia.com/qualcomm-stock-slides-on-news-of-antitrust-probe-by-chinese-regulators-11827911