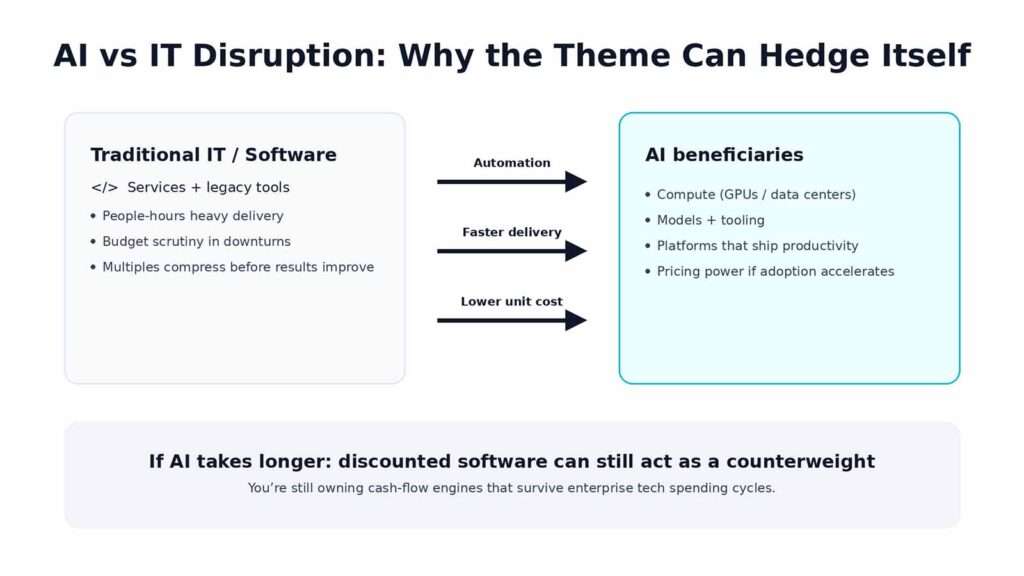

If software/IT gets disrupted, AI tends to capture the upside because the disruption is the point: automation, faster delivery, and lower unit costs. But if the “AI wins immediately” thesis turns out wrong (or just takes longer), buying quality software/IT at discounted valuations can act like an internal counterweight—because you’re still owning the cash-flow engines that power enterprise tech spending. That’s the core idea: don’t judge your strategy by one or two stocks; judge it by the entire portfolio theme, position sizing, and time horizon.

The mistake most people make: evaluating a theme like a single stock

A theme (AI, cloud software, Indian IT, semiconductors) behaves like a small ecosystem. One pocket can rally while another pocket bleeds—sometimes for months—without breaking the long-term logic.

What usually goes wrong is not the theme, but the expectation: people expect everything to move up together. In real markets, correlations change fast.

Here’s the practical framing:

- AI is the “disruption beneficiary” basket

- Traditional IT/software can be the “cash-flow + valuation mean reversion” basket

- Your job is to size them so the combined result is survivable during drawdowns

The core thesis: disruption can still be a hedge (yes, really)

Let’s make the idea concrete.

If AI disrupts IT services and legacy software:

- AI infrastructure and AI-native platforms can gain pricing power

- Companies shipping productivity gains can expand margins

- Demand shifts from “people hours” to “compute + models + automation”

But if AI adoption slows, regulation bites, budgets tighten, or the hype cycle deflates:

- Enterprises still need software

- Cost-cutting often pushes firms back to vendors with proven ROI

- Beaten-down IT can rebound on “less bad” results, buybacks, and stabilization

That’s why an AI portfolio hedge can exist inside tech itself: you’re not betting on one narrow outcome; you’re owning two adjacent outcomes with different drivers (growth vs turnaround/valuation).

Why your IT/software sleeve can look ugly—and still be “on plan”

In your note, you highlighted a painful reality: broad IT indices can fall hard from peaks (for example, a 30%30% drawdown from the top). Even if you didn’t buy the peak, you still feel the pain because:

- Multiples compress before earnings visibly recover

- Sentiment stays negative longer than you expect

- “turnaround” timelines slip

The key is to label the position correctly:

- If it’s a turnaround play, don’t demand growth-play behaviour

- Compare it to similar turnarounds, not to mega-cap compounders

If you buy a turnaround and then judge it against a rocket ship, you’ll always feel like you made a mistake—even when your original thesis is intact.

Portfolio construction: the part nobody wants to do (but it’s the whole game)

The most useful line in your post is: “Look at portfolios/themes in entirety.”

Here’s a practical framework to make that real.

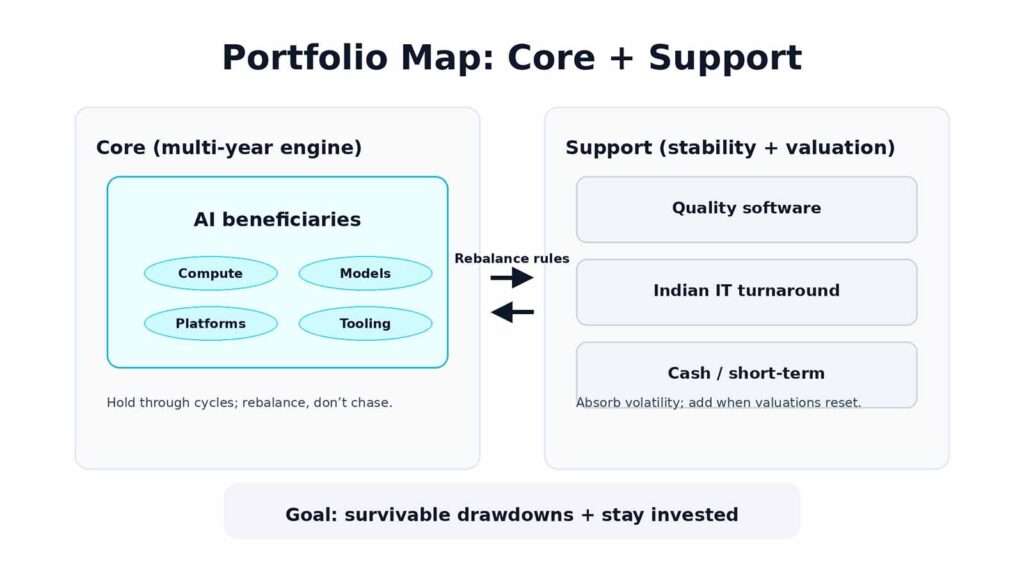

1) Decide what is “core” and what is “support”

If AI is your core (you mentioned ~80%80%), then treat it like a multi-year engine, not a trade.

Then define the support sleeve (Indian IT, US software, value-ish tech) as:

- volatility absorber (relative to frothy segments)

- valuation re-rating candidate

- dry powder destination when AI runs too hot

This is where the AI portfolio hedge becomes a process, not a slogan.

2) Set rules before the market tests you

Write down rules when you’re calm:

- Rebalance rule: “If AI sleeve grows beyond X%X%, trim to X%X% and add to laggards”

- Add-on rule: “Add only when valuation and earnings expectations reset (not just because price fell)”

- Time rule: “Turnaround sleeve gets 44–88 quarters before I judge execution”

Rules reduce panic-selling and prevent “narrative hopping.”

3) Don’t confuse diversification with diworsification

Owning 2525 random stocks isn’t diversification. It’s often just untracked risk.

A cleaner approach is fewer, well-defined buckets:

- AI beneficiaries (compute, models, AI platforms, AI tooling)

- Software/IT compounders (high retention, pricing power)

- Turnaround/value tech (where expectations are already low)

- Non-tech ballast (optional, but helpful if you can’t stomach drawdowns)

A realistic example allocation (for an aggressive tech investor)

Not advice—just an illustration of how you might express your logic.

- 60%60% AI beneficiaries (the growth engine)

- 20%20% quality software/platform names (durable cash flows)

- 10%10% Indian IT turnaround basket (mean reversion + buybacks)

- 10%10% cash or short-term debt fund (ammo + emotional stability)

Notice this still keeps AI dominant, but reduces the “all-weather” fragility that shows up when one trade gets crowded.

If you truly want 80%80% AI exposure, then consider reducing single-stock concentration inside that 80%80% by spreading across sub-segments instead of doubling down on one storyline.

Why this market feels harder than before

Your examples are the right mental model: large drawdowns are no longer “rare events.”

- Silver can correct sharply after hype or positioning unwinds

- Bitcoin can fall 50%50%–60%60% in a typical cycle

- Popular mega-caps can go sideways for years

- Equity indices can deliver disappointing real returns even when headlines feel bullish

None of that automatically means your strategy is broken. It means your strategy must assume pain as the entry fee.

A simple test: if a 25%25% drawdown in one sleeve breaks your discipline, then the sleeve is too large for your temperament (even if the thesis is right).

How to talk about “getting crushed” without losing the plot

When your non-AI sleeve drops, here are the questions that keep you rational:

- Did the original reason for buying change, or only the price?

- Is management executing (deal wins, margins, guidance stability), or deteriorating?

- Are you seeing temporary compression (valuation) or permanent impairment (business model)?

- Would you buy the same asset today at today’s price, given the updated facts?

If the answers remain supportive, the drawdown is painful but not necessarily fatal.

Make it easier to track: a one-page “theme dashboard”

This is how you avoid “1–2 stocks doing well/bad” thinking.

Create a small dashboard (Notion/Sheet) with:

- Sleeve weights (AI, software, IT turnaround, cash)

- Average buy price and thesis bullet points per sleeve

- “Thesis health” notes each quarter (2–3 lines, not essays)

- A rebalancing trigger line (set it once, follow it)

This is the boring part that makes your results look “lucky” later.

A personal note on honesty

If you’re telling a community to hold what you hold, the strongest trust-builder is consistency: you take the same hits, you follow the same rules, and you explain the same framework when markets are messy. That’s what separates “signals” from performance-chasing.

Also: beating a benchmark is great, but the repeatable edge is process—allocation, patience, and rebalancing—not one hot pick.

Risk disclaimer

This is educational and reflects one way to think about themes and position sizing. It is not financial advice. Markets can stay irrational longer than you can stay comfortable, and concentrated portfolios can face large drawdowns.

👉 You Might also find this post insightful – https://bosslevelfinance.com/should-you-invest-in-ai-chip-leader-right-now

Source links (for further reading)

https://www.nseindia.com/market-data/indices

https://www.niftyindices.com/indices/equity/sectoral-indices/nifty-it

https://www.sebi.gov.in/investors.html

https://www.tradingview.com/

https://finance.yahoo.com/

https://www.lbma.org.uk/prices-and-data/precious-metal-prices

https://coinmarketcap.com/

https://www.nasdaq.com/market-activity/index/comp