Money stress affects millions of Americans today. However, with smart planning and the right strategies, you can break free from the paycheck-to-paycheck cycle. Furthermore, achieving financial freedom in 2025 is more attainable than ever before. Additionally, this comprehensive guide will show you exactly how much to earn, save, and invest to retire early and live life on your terms.

Financial Freedom: How Much Is “Enough” in 2025?

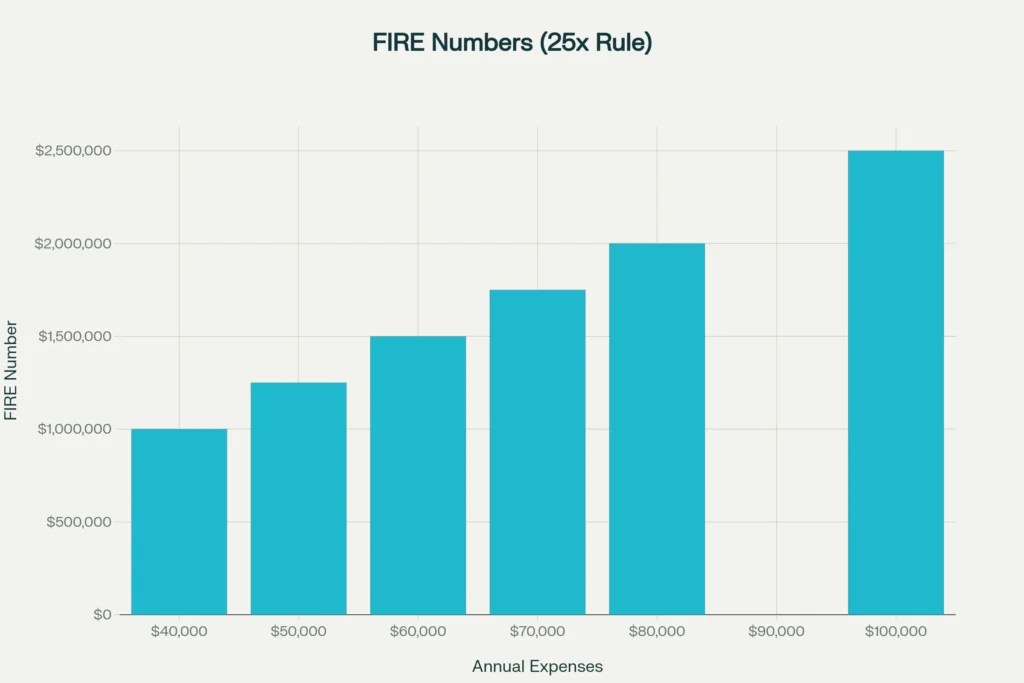

The classic rule of thumb is simple: target 25x annual expenses to reach financial independence, which aligns with the well-known 4% initial withdrawal guideline studied over 30-year retirements. If annual spending is $50,000, the independence target is about $1.25 million. However, if planning for very long retirements (40–50 years), consider using a lower initial withdrawal rate (around 3–3.5%) to improve safety margins.

- 25x expenses and a 4% initial withdrawal rate were historically successful over 30 years with balanced stock/bond mixes, per Trinity/Bengen-style analyses.

- For 40–50 years, research and modern replications suggest leaning toward 3–3.5% for higher confidence over longer horizons.

Where Income Stands Today (So You Can Plan Realistically)

As a planning anchor, the latest U.S. Census report shows real median household income at $80,610 in 2023, the most recent official data point available as of 2025. Using this as the starting point helps build realistic savings rates and budgets for a 2025 plan.

- This is a national median; individual paths vary by state, job, and household size.

The Saving Rate: Your Fastest Lever to Financial Freedom

Because investment compounding works best on big, consistent contributions, raising the savings rate often matters more than chasing higher returns. While exact timelines depend on market behavior, the principle is durable: increase savings rate, reduce years to independence.

- Keep fixed costs lean (housing, transport, food), so savings can rise even if income grows.

- Automate investing into broad, low-cost index funds to stay consistent through cycles.

Investing: Sensible, Diversified, Long-Term

History shows the S&P 500’s long-run average annual return has been around 10–10.4% nominal since 1957, or roughly 6.5% after inflation, though year-to-year results swing widely. That’s why simple, diversified, low-cost exposure—paired with an adequate cash buffer—supports most financial freedom plans.

- Long-run context: ~10.33–10.4% nominal average annual return since 1957; ~6.5% real.

- Returns vary a lot annually; for example, total returns were 26.29% in 2023 and 25.02% in 2024, reminding us not to rely on any single year.

How Much Should You Earn and Save to Retire Early?

Rather than rely on shaky “by-age” averages, build a plan that scales with expenses and time horizon, then choose a withdrawal rate that matches risk tolerance and retirement length.

- Step 1: Estimate annual spending (e.g., $40,000, $60,000, $80,000).

- Step 2: Choose an initial withdrawal rate based on horizon: 4% for ~30 years; consider 3–3.5% for 40–50 years.

- Step 3: Calculate the target:

– $40,000 spending → ~$1.0M at 4%; ~$1.14–$1.33M at 3.5–3%.

– $60,000 spending → ~$1.5M at 4%; ~$1.71–$2.0M at 3.5–3%.

– $80,000 spending → ~$2.0M at 4%; ~$2.29–$2.67M at 3.5–3%.

- Step 4: Back into savings needs using the current income reference point (e.g., median $80,610) and raise savings rate via lifestyle design and side income, not just salary jumps.

Because market paths differ, consider building in buffers: partial work, flexible spending, and a cash cushion to reduce sequence risk in early years of retirement.

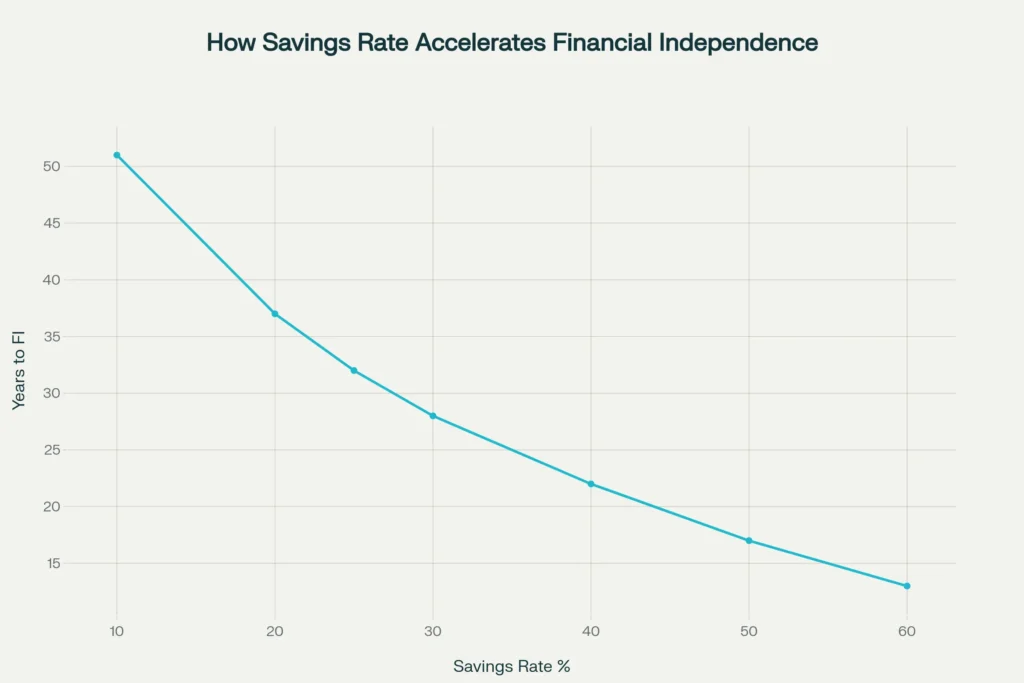

The Power of Savings Rate: Your Fast Track to Financial Freedom

Savings rate vs years to achieve financial independence – higher savings rates dramatically reduce the time needed

Your savings rate determines how quickly you’ll reach financial freedom. Importantly, most Americans save only 10-15% of their income. However, FIRE enthusiasts save 50-70% of their earnings.

Why Higher Savings Rates Matter

Consider these timeline examples:

10% savings rate: 51 years to reach financial freedom

25% savings rate: 32 years to independence

50% savings rate: Only 17 years needed

60% savings rate: Just 13 years required

Therefore, every percentage point increase in your savings rate dramatically cuts years off your working life. Additionally, this explains why FIRE followers prioritize aggressive saving over lifestyle inflation.

Things to consider before beginning the journey

- Track 3 months of spending, annualize, and pick a target withdrawal rate aligned with retirement length and risk preference.

- Automate contributions into low-cost, diversified stock/bond funds; add REIT exposure or international diversification based on risk tolerance and goals.

- Build a 6–12 month emergency fund to avoid selling assets in down markets.

- Revisit annually: reset contributions, confirm asset allocation, and rebalance if needed

The 4% Safe Withdrawal Rule Explained

Once you reach your FIRE number, you can safely withdraw 4% annually. For instance, a $1.5 million portfolio generates $60,000 per year in retirement income. Moreover, this withdrawal rate historically preserves your principal over 30+ year periods.

What About Location and Costs?

Costs vary a lot by state and city, which affects how big a portfolio is required; rather than rely on a generic list, compare personal expenses where living now versus a lower-cost region and recalculate the FIRE number accordingly. Using 2023 state income medians and local cost-of-living data will make the plan more precise for 2025 decisions.

- Use the national $80,610 median only as a context anchor; your actual income and spending drive the real plan.

- Geographic arbitrage works if it truly lowers housing, taxes, and healthcare while keeping lifestyle acceptable.

Current Market Conditions in 2025

The S&P 500 has gained 9.47% year-to-date in 2025. Meanwhile, inflation remains moderate at 2.7% as of June 2025. Consequently, real returns continue supporting long-term wealth building strategies.

Creating Multiple Income Streams for Faster Financial Freedom

Relying on just your salary limits your wealth-building potential. Instead, successful FIRE achievers develop multiple income sources. Additionally, side hustles have become increasingly profitable in 2025.

Side Hustle Income Statistics

Recent data shows promising earning potential:

- Average monthly side hustle income: $891 per month

- Millennials earn the most: $1,129 monthly average

- 36% of Americans have side gigs

- Global gig economy valued at: $556.7 billion in 2024

Furthermore, popular side hustles include:

- Freelance writing and consulting

- E-commerce and dropshipping

- Real estate investment (REITs)

- Online course creation

- Delivery and gig work

Therefore, diversifying your income significantly accelerates your journey to financial freedom.

Real Estate Investment Trusts: Passive Income for Financial Freedom

REITs offer an excellent way to generate passive income without direct property ownership. Additionally, many REITs pay attractive dividend yields ranging from 4-8% annually. Moreover, companies like Realty Income (nicknamed “The Monthly Dividend Company”) provide steady monthly payments.

Benefits of REIT Investing

- High dividend yields: Often 4-8% annually

- Monthly income: Some REITs pay monthly dividends

- Professional management: No direct property responsibilities

- Liquidity: Easily bought and sold like stocks

- Diversification: Access to various property types

Consequently, REITs form an important component of many FIRE portfolios. Furthermore, they provide inflation protection through real estate appreciation.

Most Affordable States for Early Retirement

- West Virginia: $58,000 annual retirement costs

- Oklahoma: $60,000 annual retirement costs

- Kansas: Similar low-cost structure

- Nebraska: Excellent healthcare and low costs

- Florida: No state income tax plus warm weather

Meanwhile, expensive states require much higher FIRE numbers:

- Hawaii: $129,296 annual retirement costs

- California: High taxes and living expenses

- New York: Highest state tax burden

- Massachusetts: Over $70,000 annual retirement costs

Therefore, geographic arbitrage can significantly reduce your required FIRE number. Additionally, some people achieve financial freedom faster by relocating to lower-cost areas.

Your 2025 Action Plan for Financial Freedom

Success requires a systematic approach to building wealth. Moreover, starting immediately gives you the greatest advantage due to compound growth.

Step 1: Calculate Your Personal FIRE Number

First, track your annual expenses for three months. Then, multiply by 25 to find your target savings amount. Additionally, consider whether you want “Lean FIRE” (minimal expenses) or “Fat FIRE” (comfortable lifestyle).

Step 2: Maximize Your Savings Rate

Next, audit every expense category ruthlessly. Furthermore, aim to save at least 50% of your income through:

- Housing cost optimization (house hacking, roommates)

- Transportation efficiency (reliable used cars, cycling)

- Food cost reduction (meal planning, cooking at home)

- Entertainment alternatives (free activities, library resources)

Step 3: Invest Aggressively in Low-Cost Index Funds

Subsequently, invest your savings in diversified index funds. Additionally, focus on:

- Total stock market index funds (VTSAX, FZROX)

- International diversification (VTIAX, FTIHX)

- Real estate exposure through REITs (VNQ, SCHH)

- Bond allocation based on age (BND, FXNAX)

Step 4: Develop Side Income Streams

Meanwhile, build multiple income sources to accelerate progress. Furthermore, consider your skills and interests when choosing side hustles. Additionally, online opportunities offer the greatest scalability potential.

Step 5: Monitor and Adjust Regularly

Finally, review your progress quarterly and adjust strategies accordingly. Moreover, stay informed about tax law changes and investment opportunities. Additionally, consider working with a fee-only financial advisor for complex situations.

Common Mistakes That Derail Financial Freedom Plans

Even with good intentions, many people make costly errors. Additionally, avoiding these mistakes keeps you on track toward early retirement.

Lifestyle Inflation Trap

As income increases, many people automatically increase spending proportionally. However, this prevents savings rate growth and delays financial freedom. Instead, maintain fixed expenses while investing salary increases.

Insufficient Emergency Fund

Inadequately, some FIRE enthusiasts invest everything without maintaining emergency reserves. Nevertheless, unexpected expenses can force early withdrawals from investment accounts. Therefore, maintain 6-12 months of expenses in cash savings.

Tax Inefficiency

Furthermore, ignoring tax optimization costs thousands annually. Additionally, maximize tax-advantaged accounts like 401(k)s, IRAs, and HSAs before taxable investing. Moreover, consider Roth conversions during low-income years.

The Psychology of Financial Freedom: Staying Motivated

Mental preparation proves just as important as financial planning. Additionally, the journey to financial freedom requires significant lifestyle changes and delayed gratification.

Building Sustainable Habits

Success comes from consistent daily actions rather than occasional dramatic changes. Furthermore, automate investments to remove emotional decision-making. Additionally, celebrate small milestones to maintain motivation throughout the journey.

Finding Your “Why”

Clearly define what financial freedom means personally to you. Moreover, visualize your ideal retirement lifestyle regularly. Additionally, connect emotionally with your long-term goals to overcome short-term temptations.

Looking Ahead: Financial Freedom Beyond 2025

Economic conditions will continue evolving, but fundamental principles remain constant. Additionally, technology creates new opportunities for income generation and cost reduction. Furthermore, the FIRE movement continues growing as more people prioritize freedom over consumption.

Preparing for Economic Changes

Diversification across asset classes, geographies, and income sources provides resilience against uncertainty. Moreover, maintaining flexibility in your plans allows adaptation to changing circumstances. Additionally, continuous learning ensures you stay ahead of economic trends.

Financial freedom in 2025 remains achievable for those willing to make necessary sacrifices and strategic decisions. Furthermore, starting today gives you the maximum benefit from compound growth and time. Additionally, remember that the path requires discipline, but the destination offers ultimate freedom to live life on your terms.

You Might also find this post insightful – https://bosslevelfinance.com/qqqm-quietly-soaring-the-secret-etf-winners-are-adding-now

Disclaimer: This analysis is for educational purposes only. We do not encourage users to buy, sell, or hold any specific investments. Stock markets are subject to change and past performance does not guarantee future results. Please conduct your own due diligence and consult with qualified financial professionals before making investment decisions.

Sources:

U.S. Bureau of Labor Statistics – Consumer Price Index and Employment Data

Vanguard “How America Saves 2025” Report

Fidelity Investments Retirement Analysis Q1 2025

Trading Economics – US Inflation Data

Federal Reserve Economic Data (FRED)

Census Bureau – Median Household Income Reports

Morningstar Retirement Research

NerdWallet FIRE Movement Analysis

Investopedia Financial Independence Research

Visual Capitalist – Retirement Cost Analysis by State

- https://worldpopulationreview.com/state-rankings/median-household-income-by-state

- https://www.kiplinger.com/retirement/401ks/the-average-401k-balance-by-age

- https://www.awjlaw.com/research/retirement-report-2025-best-worst-states-to-retire/

- https://www.justice.gov/ust/eo/bapcpa/20241101/bci_data/median_income_table.htm

- https://www.bankrate.com/retirement/average-401k-balance-by-age/

- https://www.westernsouthern.com/retirement-readiness-index

- https://en.wikipedia.org/wiki/Household_income_in_the_United_States

- https://www.investopedia.com/articles/personal-finance/010616/whats-average-401k-balance-age.asp

- https://www.visualcapitalist.com/mapped-annual-retirement-costs-by-state/

- https://www.census.gov/library/visualizations/2024/comm/median-household-income.html

- https://www.cnbc.com/select/average-401k-balance-by-age/

- https://www.the-ifw.com/blog/lifestyle-wellness/most-affordable-states-to-retire-in-2025/

- https://www.census.gov/topics/income-poverty/income.html

- https://www.fidelity.com/learning-center/personal-finance/average-retirement-savings

- https://www.cpf.gov.sg/service/article/how-much-is-my-full-retirement-sum

- https://www.census.gov/library/publications/2024/demo/p60-282.html

- https://www.fidelity.com/learning-center/smart-money/average-net-worth-by-age

- https://www.bankrate.com/retirement/best-and-worst-states-for-retirement/

- https://fred.stlouisfed.org/series/MEHOINUSA672N

- https://www.empower.com/the-currency/life/average-401k-balance-age

- https://tradingeconomics.com/united-states/inflation-cpi

- https://www.slickcharts.com/sp500/returns

- https://www.stashaway.hk/r/combining-the-50-30-20-budget-rule-and-fire

- https://www.cnbc.com/2025/06/11/cpi-inflation-may-2025.html

- https://ycharts.com/indicators/sp_500_monthly_return

- https://www.nerdwallet.com/article/investing/financial-independence-retire-early

- https://tradingeconomics.com/united-states/consumer-price-index-cpi

- https://www.investopedia.com/ask/answers/042415/what-average-annual-return-sp-500.asp

- https://www.baloise.lu/en/blog/money-future/2025/early-retirement-fire.html

- https://www.usinflationcalculator.com/inflation/current-inflation-rates/

- https://in.investing.com/indices/us-spx-500-historical-data

- https://en.wikipedia.org/wiki/FIRE_movement

- https://www.bls.gov/news.release/cpi.nr0.htm

- https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

- https://www.gripinvest.in/blog/financial-independence-retire-early-fire

- https://www.bls.gov/news.release/pdf/cpi.pdf

- https://finance.yahoo.com/quote/%5EGSPC/history/

- https://www.investopedia.com/terms/f/financial-independence-retire-early-fire.asp

- https://www.investing.com/economic-calendar/cpi-733

- https://www.macrotrends.net/2526/sp-500-historical-annual-returns

- https://smartasset.com/retirement/the-average-salary-by-age

- https://www.hostinger.com/tutorials/side-hustle-statistics

- https://www.morningstar.com/stocks/best-reits-buy

- https://www.youtube.com/watch?v=wquyCAJ0j6Y

- https://magecomp.com/blog/best-side-hustles/

- https://www.smallcase.com/lists/reit-stocks/

- https://dqydj.com/average-median-top-salary-by-age-percentiles/

- https://www.buzzfeed.com/jake_farrington/high-paying-side-hustles

- https://www.nerdwallet.com/article/investing/reit-investing

- https://www.indeed.com/career-advice/pay-salary/average-salary-by-age

- https://www.shopify.com/blog/side-hustle

- https://www.icicidirect.com/fd-and-bonds/real-estate-investment-trust

- https://www.forbes.com/advisor/in/business/average-salary-by-age/

- https://www.nerdwallet.com/article/finance/how-to-make-money

- https://groww.in/p/real-estate-investment-trust-reit

- https://www.bls.gov/charts/usual-weekly-earnings/usual-weekly-earnings-current-quarter-by-age.htm

- https://www.flexjobs.com/blog/post/remote-side-jobs-done-from-home-hiring-now-2

- https://www.tickertape.in/stocks/collections/reit-stocks

- https://www.upgrad.com/study-abroad/articles/average-salary-in-usa/

- https://www.coursera.org/articles/side-hustles-from-home