The Walt Disney Company stands at a fascinating crossroads in October 2025. Moreover, this entertainment giant has captured investors’ attention with its remarkable transformation. Furthermore, the company’s stock performance tells a compelling story of resilience and strategic evolution.

Current Stock Performance: The Numbers Tell A Story

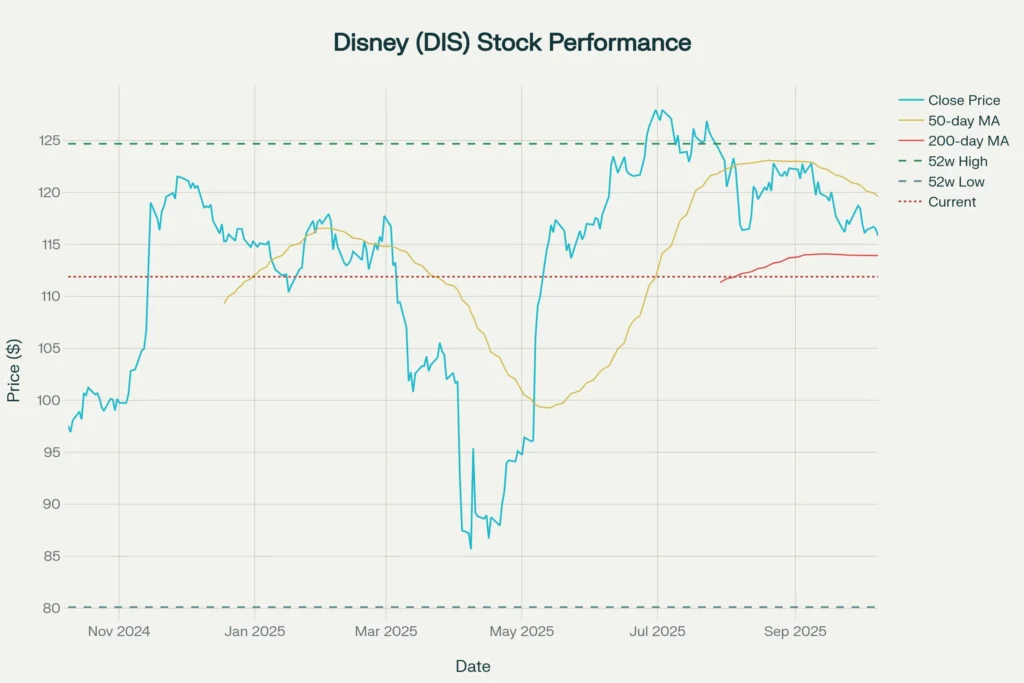

Disney’s stock currently trades at $111.89, representing a solid 19.5% gain over the past year. Additionally, this performance significantly outpaces many entertainment peers. However, recent months have shown some volatility, with the stock declining 5.3% in the last 30 days.

The company’s market capitalization now stands at an impressive $201.4 billion. Meanwhile, trading volumes remain robust at approximately 9.4 million shares daily. Furthermore, the stock’s 52-week range of $80.10 to $124.69 demonstrates significant price movement throughout the year.

Financial Health: Strong Fundamentals Drive Growth

Disney’s financial performance in 2024 shows remarkable improvement across key metrics. Specifically, the company generated $91.4 billion in revenue, marking a 2.8% increase from 2023. Most importantly, net income surged dramatically to $5.0 billion, more than doubling from the previous year’s $2.4 billion.

The company’s operating margin expanded to 13.0% in 2024, compared to 10.1% in 2023. Similarly, net profit margins improved to 5.4% from 2.6%. These improvements clearly demonstrate Disney’s operational efficiency gains.

Key Financial Metrics Breakdown:

- Revenue Growth: 2.8% year-over-year

- Operating Margin: 13.0% (improved from 10.1%)

- Net Margin: 5.4% (improved from 2.6%)

- Earnings Per Share: $2.72 (up from $1.29)

Business Segments: Diversified Revenue Streams

Entertainment Division: Streaming Success

Disney’s Direct-to-Consumer segment achieved a significant milestone by reaching profitability of $346 million. Additionally, the company now boasts 183 million Disney+ and Hulu subscriptions. Furthermore, this represents steady growth of 2.6 million subscribers quarter-over-quarter.

The integration of Disney+, Hulu, and ESPN into a unified platform creates tremendous value. Moreover, this strategy reduces churn rates while increasing user engagement. Consequently, average revenue per subscriber continues to climb.

Experiences Division: Theme Park Renaissance

Disney’s Experiences segment delivered outstanding performance with $2.5 billion in operating income. Notably, domestic parks saw a 22% increase in operating income. Furthermore, the company maintains ambitious expansion plans worldwide, including new cruise ships and international parks.

The division benefits from strong consumer spending on experiences. Additionally, Disney’s pricing power remains evident through consistent per-capita spending increases. Moreover, the company’s global expansion strategy targets emerging markets with growing middle classes.

Sports Segment: ESPN Evolution

The Sports division generated $1.0 billion in operating income, reflecting strong year-over-year growth. However, this segment faces challenges from cord-cutting trends. Nevertheless, Disney’s planned direct-to-consumer ESPN service represents a strategic pivot toward digital distribution.

Analyst Outlook: Strong Buy Consensus

Wall Street analysts maintain overwhelmingly positive sentiment toward Disney stock. Specifically, 22 analysts provide coverage with a Strong Buy consensus. Additionally, the average price target sits at $138.53, suggesting 23.8% upside potential.

Analyst Price Targets:

- Highest Target: $159.00 (42% upside)

- Average Target: $138.53 (24% upside)

- Lowest Target: $123.00 (10% upside)

Goldman Sachs analyst Michael Ng maintains a Buy rating with a $152 price target. Similarly, Needham’s Laura Martin recommends a Buy with a $125 target. Furthermore, Bernstein analyst Laurent Yoon supports an Outperform rating at $129.

Valuation Analysis: Attractive Entry Point

Disney’s current valuation appears compelling compared to historical levels. The stock trades at a P/E ratio of 17.5x, significantly below the entertainment industry average of 28x. Moreover, this discount suggests potential for multiple expansion.

Several factors support the undervaluation thesis:

- Strong brand portfolio and intellectual property

- Diversified revenue streams across multiple segments

- Improving operational efficiency and margins

- Strategic digital transformation initiatives

Investment Thesis: Why Disney Deserves Your Attention

Strengths Supporting A Buy Rating

Brand Power: Disney possesses unmatched intellectual property assets. Additionally, franchises like Marvel, Star Wars, and Pixar generate consistent revenue across multiple platforms. Furthermore, these properties provide sustainable competitive advantages.

Streaming Transformation: The company successfully achieved Direct-to-Consumer profitability. Moreover, subscriber growth continues steadily despite industry headwinds. Furthermore, content integration strategies enhance user retention and pricing power.

Experiences Growth: Theme park expansions drive long-term revenue growth. Additionally, international markets offer significant expansion opportunities. Moreover, Disney’s pricing power in experiences remains robust.

Financial Recovery: Margin expansion demonstrates operational improvements. Furthermore, strong cash flow generation supports dividend payments and share buybacks. Additionally, balance sheet strength provides strategic flexibility.

Risks To Consider

Streaming Competition: Netflix, Amazon Prime, and other platforms intensify competition. Moreover, content costs continue rising across the industry. Furthermore, consumer subscription fatigue poses growth challenges.

Economic Sensitivity: Theme parks face cyclical demand patterns. Additionally, consumer discretionary spending affects multiple segments. Moreover, global economic uncertainty impacts international operations.

Content Costs: Sports broadcasting rights escalate rapidly. Furthermore, original content production requires significant investments. Additionally, talent costs continue increasing industry-wide.

Technical Analysis: Chart Patterns Signal Opportunity

The stock recently tested support near $110-$112 levels. Additionally, this area coincides with the 50-day moving average. Furthermore, any bounce from current levels could target the $120-$125 resistance zone.

Key technical levels include:

- Support: $110-$112 (current trading range)

- Resistance: $120-$125 (previous highs)

- Breakout Target: $130+ (analyst average target)

Volume patterns suggest accumulation at lower levels. Moreover, institutional buying appears evident during recent weakness. Furthermore, options activity indicates bullish positioning among sophisticated investors.

Investment Recommendation: Strategic Buy

Based on comprehensive analysis, Disney merits a Strong Buy recommendation for several compelling reasons:

Why Buy Disney Now:

- Attractive Valuation: Trading at 17.5x P/E versus industry average of 28x

- Operational Improvements: Expanding margins across all segments

- Streaming Profitability: Direct-to-Consumer segment reached profitability

- Analyst Support: Strong Buy consensus with 24% average upside

- Brand Strength: Unmatched intellectual property portfolio

Target Price And Timeline:

- 12-Month Price Target: $138-$145

- Expected Return: 23-30% potential upside

- Risk Level: Moderate (established business model)

- Investment Horizon: Long-term (2-3 years optimal)

Position Sizing Recommendation:

Conservative investors should consider a 2-3% portfolio allocation. Meanwhile, growth-oriented investors might target 4-5% allocation. Furthermore, dollar-cost averaging into positions makes sense given current volatility.

Conclusion: The Magic Continues

Disney represents a compelling investment opportunity in today’s market environment. Moreover, the company successfully navigated pandemic challenges while strengthening its competitive position. Furthermore, multiple catalysts support continued stock appreciation.

The combination of streaming profitability, theme park recovery, and operational improvements creates a powerful investment thesis. Additionally, attractive valuation levels provide downside protection. Most importantly, Disney’s unmatched brand portfolio ensures long-term competitive advantages.

For investors seeking exposure to entertainment, streaming, and experiences sectors, Disney offers diversified growth potential. Furthermore, the company’s transformation story remains in early stages. Consequently, patient investors should benefit from continued value creation.

Final Recommendation: Buy Disney stock for long-term portfolios, with price targets of $138-$145 representing 23-30% upside potential over the next 12 months.

👉 You Might also find this post insightful – https://bosslevelfinance.com/should-you-consider-investing-in-uipath-stock-now

👉 Create a Vested Account today to start investing in US Stocks – https://refer.vestedfinance.com/RUKU88007

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. We do not encourage users to buy, sell, or hold any securities. Stock markets are subject to change and past performance does not guarantee future results. Always conduct your own due diligence and consult with qualified financial advisors before making investment decisions.

Sources:

- https://simplywall.st/stocks/us/media/nyse-dis/walt-disney/news/how-the-streaming-subscriber-dip-impacts-disneys-current-val

- https://thewaltdisneycompany.com/the-walt-disney-company-reports-third-quarter-and-nine-months-earnings-for-fiscal-2025/

- https://www.tipranks.com/stocks/dis/forecast

- https://www.nasdaq.com/articles/3-reasons-hold-disney-stock-now-despite-231-surge-6-months

- https://thewaltdisneycompany.com/app/uploads/2025/08/q3-fy25-earnings.pdf

- https://stockanalysis.com/stocks/dis/forecast/

- https://finance.yahoo.com/news/fresh-look-disney-dis-valuation-131418136.html

- https://finance.yahoo.com/news/walt-disney-company-reports-third-104000004.html

- https://in.tradingview.com/symbols/NYSE-DIS/forecast/

- https://finance.yahoo.com/news/does-disney-subscriber-loss-mean-042740079.html

- https://www.linkedin.com/pulse/walt-disney-company-q3-fy25-earnings-analysis-8625-faisal-amjad-rptqf

- https://www.marketbeat.com/stocks/NYSE/DIS/forecast/

- https://stockanalysis.com/stocks/dis/

- https://thewaltdisneycompany.com/investor-relations/

- https://www.marketwatch.com/investing/stock/dis/analystestimates

- https://in.investing.com/analysis/disney-from-sleeping-beauty-to-a-35-jump-magic-was-in-the-numbers-all-along-200631503

- https://www.cnbc.com/2025/08/06/disney-dis-earnings-q3-2025.html

- https://finance.yahoo.com/quote/DIS/analysis/

- https://www.marketbeat.com/instant-alerts/filing-the-walt-disney-company-dis-position-trimmed-by-us-bancorp-de-2025-10-09/

- https://www.statista.com/statistics/224397/quarterly-revenue-of-the-walt-disney-company/

https://www.statista.com/statistics/224397/quarterly-revenue-of-the-walt-disney-company/The combination of streaming profitability, theme park recovery, and operational improvements creates a powerful investment thesis. Additionally, attractive valuation levels provide downside protection. Most importantly, Disney’s unmatched brand portfolio ensures long-term competitive advantages.

https://www.tipranks.com/stocks/dis/forecast

https://www.nasdaq.com/articles/3-reasons-hold-disney-stock-now-despite-231-surge-6-months

https://thewaltdisneycompany.com/app/uploads/2025/08/q3-fy25-earnings.pdf

https://stockanalysis.com/stocks/dis/forecast/

https://finance.yahoo.com/news/fresh-look-disney-dis-valuation-131418136.html

https://finance.yahoo.com/news/walt-disney-company-reports-third-104000004.html

https://in.tradingview.com/symbols/NYSE-DIS/forecast/

https://finance.yahoo.com/news/does-disney-subscriber-loss-mean-042740079.html

https://www.linkedin.com/pulse/walt-disney-company-q3-fy25-earnings-analysis-8625-faisal-amjad-rptqf

https://www.marketbeat.com/stocks/NYSE/DIS/forecast/

https://stockanalysis.com/stocks/dis/

https://thewaltdisneycompany.com/investor-relations/

https://www.marketwatch.com/investing/stock/dis/analystestimates

https://www.cnbc.com/2025/08/06/disney-dis-earnings-q3-2025.html

https://finance.yahoo.com/quote/DIS/analysis/

For investors seeking exposure to entertainment, streaming, and experiences sectors, Disney offers diversified growth potential. Furthermore, the company’s transformation story remains in early stages. Consequently, patient investors should benefit from continued value creation.

Final Recommendation: Buy Disney stock for long-term portfolios, with price targets of $138-$145 representing 23-30% upside potential over the next 12 months.

Sources:

- https://simplywall.st/stocks/us/media/nyse-dis/walt-disney/news/how-the-streaming-subscriber-dip-impacts-disneys-current-val

- https://thewaltdisneycompany.com/the-walt-disney-company-reports-third-quarter-and-nine-months-earnings-for-fiscal-2025/

- https://www.tipranks.com/stocks/dis/forecast

- https://www.nasdaq.com/articles/3-reasons-hold-disney-stock-now-despite-231-surge-6-months

- https://thewaltdisneycompany.com/app/uploads/2025/08/q3-fy25-earnings.pdf

- https://stockanalysis.com/stocks/dis/forecast/

- https://finance.yahoo.com/news/fresh-look-disney-dis-valuation-131418136.html

- https://finance.yahoo.com/news/walt-disney-company-reports-third-104000004.html

- https://in.tradingview.com/symbols/NYSE-DIS/forecast/

- https://finance.yahoo.com/news/does-disney-subscriber-loss-mean-042740079.html

- https://www.linkedin.com/pulse/walt-disney-company-q3-fy25-earnings-analysis-8625-faisal-amjad-rptqf

- https://www.marketbeat.com/stocks/NYSE/DIS/forecast/

- https://stockanalysis.com/stocks/dis/

- https://thewaltdisneycompany.com/investor-relations/

- https://www.marketwatch.com/investing/stock/dis/analystestimates

- https://in.investing.com/analysis/disney-from-sleeping-beauty-to-a-35-jump-magic-was-in-the-numbers-all-along-200631503

- https://www.cnbc.com/2025/08/06/disney-dis-earnings-q3-2025.html

- https://finance.yahoo.com/quote/DIS/analysis/

- https://www.marketbeat.com/instant-alerts/filing-the-walt-disney-company-dis-position-trimmed-by-us-bancorp-de-2025-10-09/

- https://www.statista.com/statistics/224397/quarterly-revenue-of-the-walt-disney-company/

- https://simplywall.st/stocks/us/media/nyse-dis/walt-disney/news/how-the-streaming-subscriber-dip-impacts-disneys-current-val

- https://thewaltdisneycompany.com/the-walt-disney-company-reports-third-quarter-and-nine-months-earnings-for-fiscal-2025/

- https://www.tipranks.com/stocks/dis/forecast

- https://www.nasdaq.com/articles/3-reasons-hold-disney-stock-now-despite-231-surge-6-months

- https://thewaltdisneycompany.com/app/uploads/2025/08/q3-fy25-earnings.pdf

- https://stockanalysis.com/stocks/dis/forecast/

- https://finance.yahoo.com/news/fresh-look-disney-dis-valuation-131418136.html

- https://finance.yahoo.com/news/walt-disney-company-reports-third-104000004.html

- https://in.tradingview.com/symbols/NYSE-DIS/forecast/

- https://finance.yahoo.com/news/does-disney-subscriber-loss-mean-042740079.html

- https://www.linkedin.com/pulse/walt-disney-company-q3-fy25-earnings-analysis-8625-faisal-amjad-rptqf

- https://www.marketbeat.com/stocks/NYSE/DIS/forecast/

- https://stockanalysis.com/stocks/dis/

- https://thewaltdisneycompany.com/investor-relations/

- https://www.marketwatch.com/investing/stock/dis/analystestimates

- https://in.investing.com/analysis/disney-from-sleeping-beauty-to-a-35-jump-magic-was-in-the-numbers-all-along-200631503

- https://www.cnbc.com/2025/08/06/disney-dis-earnings-q3-2025.html

- https://finance.yahoo.com/quote/DIS/analysis/

- https://www.marketbeat.com/instant-alerts/filing-the-walt-disney-company-dis-position-trimmed-by-us-bancorp-de-2025-10-09/

- https://www.statista.com/statistics/224397/quarterly-revenue-of-the-walt-disney-company/