Pfizer (PFE) stock analysis reveals compelling opportunities for 2025 despite recent volatility. Currently trading at $27.08, the pharmaceutical giant shows strong fundamentals with $14.65 billion quarterly revenue and robust dividend yields of 6.8%. Recent partnerships and strategic acquisitions position this healthcare stock for potential growth. However, patent challenges and market competition create risks that investors must understand. This comprehensive analysis explores whether this big pharma investment deserves a place in your portfolio.

Current Market Position: Where PFE Stands Today

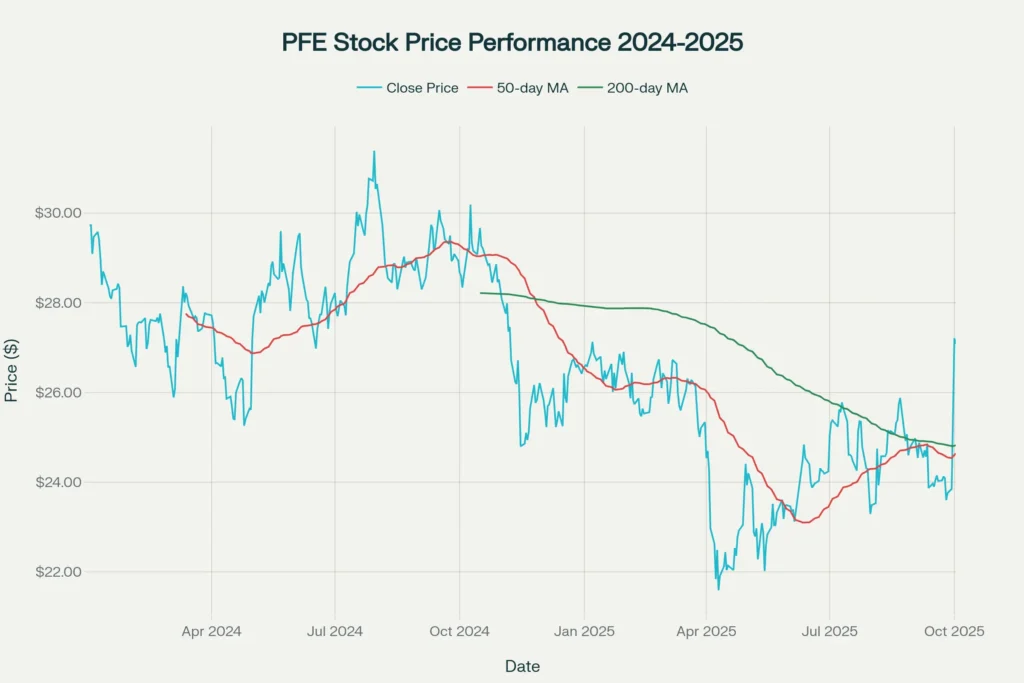

The stock market position for this pharmaceutical leader reflects both challenges and opportunities. Trading above its 50-day moving average at $24.64 and 200-day moving average at $24.82, technical indicators suggest improving momentum.

Key price metrics show interesting patterns. The 52-week range spans from $20.92 to $31.54, indicating significant volatility. Year-to-date returns show -8.91%, reflecting broader healthcare sector concerns about drug pricing and patent expirations.

Recent market reactions demonstrate investor sensitivity to news. The September 30 surge of 5.3% following Trump administration agreements highlights how policy changes affect stock performance. Additionally, the company’s strategic moves in obesity drugs through acquisitions signal management’s focus on high-growth therapeutic areas.

Financial Performance of (PFE): Breaking Down the Numbers

Revenue growth tells a compelling story about operational resilience. Second quarter 2025 results showed $14.65 billion in sales, representing 10.3% year-over-year growth. This beats analyst expectations and demonstrates the company’s ability to navigate post-pandemic transitions effectively.

Profitability metrics reveal impressive recovery patterns. Net income reached $2.91 billion in Q2 2025, compared to just $0.02 billion in the same quarter of 2024. This dramatic improvement reflects better cost management and product mix optimization.

Earnings per share of $0.51 exceeded consensus estimates by $0.20, showcasing operational efficiency improvements. The company maintains strong cash generation capabilities, supporting both dividend payments and strategic investments in research and development.

Key Financial Highlights of (PFE)

The balance sheet strength provides investment security. Current ratio of 1.26 indicates adequate liquidity for operations. Debt-to-equity ratio at 0.65 suggests manageable leverage levels for a large pharmaceutical company.

Operating margins demonstrate pricing power despite generic competition. Research and development spending continues at robust levels, ensuring future product pipeline development. This investment in innovation supports long-term competitive positioning.

Investment Catalysts: What Could Drive Growth of (PFE)

Strategic partnerships create multiple growth avenues for investors seeking healthcare exposure. The recent Trump administration agreement includes $70 billion in U.S. manufacturing investments, potentially boosting domestic operations and job creation.

Obesity drug market entry through acquisitions positions the company in a rapidly expanding therapeutic area. The $7.3 billion Metsera acquisition brings promising GLP-1 compounds showing 14.1% weight loss in Phase 2 trials.

Pipeline developments in oncology continue showing promise. Collaborations with other pharmaceutical companies on cancer treatments could generate significant revenue streams. These partnerships reduce development risks while maximizing market opportunities.

Market Expansion Opportunities

International markets offer substantial growth potential for revenue diversification. Emerging markets represent 40% of international sales, providing exposure to faster-growing economies with increasing healthcare spending.

Vaccine portfolio remains strong despite reduced COVID-19 demand. Seasonal vaccine sales and new product launches support steady revenue streams. The company’s expertise in vaccine development creates competitive advantages in future health challenges.

Risk Assessment: Understanding the Challenges

Patent cliff concerns create significant headwinds for earnings growth. Key medications face generic competition as patent protections expire. The company projects approximately $0.5 billion in losses from biosimilar competition.

Regulatory environment changes pose ongoing challenges. Drug pricing pressures from government policies could impact profit margins. The Inflation Reduction Act implementation affects Medicare Part D revenues by approximately $1 billion annually.

Competition in core therapeutic areas intensifies regularly. Other pharmaceutical companies develop competing treatments, potentially reducing market share. Innovation requirements demand continuous research and development investments to maintain competitive positions.

Operational Risks

Manufacturing disruptions could affect product availability and revenue recognition. Global supply chain complexities create potential bottlenecks. However, the company’s manufacturing optimization program aims to improve efficiency and reduce costs.

Currency fluctuations impact international revenue translation. Since international sales represent significant portions of total revenue, exchange rate movements affect financial results. Management uses hedging strategies to mitigate these risks.

Analyst Perspectives: Wall Street’s View

Professional analysts maintain mixed ratings on the stock. Bank of America recently raised price targets from $28 to $30, indicating neutral outlook with modest upside potential. Morgan Stanley increased targets to $33, reflecting optimism about operational improvements.

Consensus estimates suggest earnings growth potential. Full-year 2025 guidance predicts $2.80 to $3.00 per share, representing 10% to 18% operational growth. These projections assume successful execution of cost-cutting programs.

Forward price-to-earnings ratio of 8.22 indicates potential undervaluation compared to pharmaceutical sector averages. This metric suggests market skepticism about growth prospects despite strong financial performance.

Dividend Analysis: Income Investor Considerations

Dividend sustainability remains strong with 347 consecutive quarterly payments. The current quarterly dividend of $0.43 per share provides attractive yield of 6.8% for income-focused investors.

Payout ratio analysis shows manageable levels relative to earnings generation. Strong cash flow supports dividend payments while funding research and development activities. Management’s commitment to dividend growth creates appeal for long-term holders.

Dividend growth history demonstrates consistency despite business cycle fluctuations. This reliability makes the stock attractive for retirement portfolios seeking steady income streams. Healthcare stocks often provide defensive characteristics during market volatility.

Technical Analysis: Chart Patterns and Trends

Price action shows recovery from 2024 lows near $20.92. Recent momentum above key moving averages suggests potential trend reversal. However, resistance levels around $30-31 present challenges for further gains.

Volume patterns indicate institutional interest during price movements. The September surge accompanied by high volume suggests genuine buying interest rather than technical manipulation. This participation supports price stability.

Support levels around $24-25 provide downside protection for new positions. These levels coincide with moving averages, creating technical significance for traders and investors.

Investment Strategy: Making Your Decision

Portfolio allocation considerations depend on individual risk tolerance and investment objectives. Conservative investors might appreciate dividend income and defensive characteristics. Growth-oriented investors should evaluate pipeline potential and market expansion opportunities.

Dollar-cost averaging could benefit from current volatility patterns. Regular purchases smooth out price fluctuations while building positions gradually. This strategy works particularly well with dividend-paying stocks offering reinvestment opportunities.

Timing considerations involve monitoring regulatory developments and earnings announcements. Policy changes significantly impact pharmaceutical stock prices. Staying informed about healthcare legislation helps optimize entry and exit points.

Future Outlook: What Lies Ahead for 2025

Revenue projections for 2025 range between $61-64 billion, indicating stable business performance. Management expects operational growth despite headwinds from patent expirations and pricing pressures.

Pipeline developments could provide positive surprises for patient outcomes and investor returns. Successful drug approvals expand treatment options while generating new revenue streams. The company’s research capabilities support innovation in critical therapeutic areas.

Market conditions favor established pharmaceutical companies with diverse product portfolios. Economic uncertainty increases demand for defensive investments offering steady dividends and essential products.

You Might also find this post insightful –https://bosslevelfinance.com/is-sofi-stock-the-best-bet-in-fintech-2025

Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. We do not encourage users to buy, sell, or hold any securities. Stock markets are subject to change and past performance does not guarantee future results. Please conduct your own due diligence and consult with qualified financial advisors before making investment decisions. Always consider your risk tolerance and investment objectives.

Sources:

- Economic Times: “PFE stock rises 5.3% today: Pfizer surges on Trump drug price deal”

- Yahoo Finance: “Pfizer shares rise 3% after upping profit forecast for 2025”

- CoinCodex: “Pfizer (PFE) Stock Forecast & Price Prediction 2025–2030”

- Benzinga: “Pfizer (PFE) Stock Price Prediction: 2025, 2026, 2030”

- Pfizer Official Press Releases and Financial Reports

- Morningstar: “Pfizer Stock Price Quote – NYSE: PFE”

- Investors.com: “Is Pfizer Stock A Buy After Pharma Titan Strikes A Deal”

- MarketBeat: “Pfizer Stock Price Expected to Rise, Bank of America Analyst Says”

- https://economictimes.com/news/international/us/pfe-stock-rises-5-3-today-pfizer-surges-on-trump-drug-price-deal-70b-u-s-investment-and-7-3b-metsera-weight-loss-acquisition-boosting-obesity-market-outlook/articleshow/124239938.cms

- https://finance.yahoo.com/news/pfizer-shares-rise-3-upping-165038961.html

- https://coincodex.com/stock/PFE/price-prediction/

- https://www.benzinga.com/money/pfizer-stock-price-prediction

- https://www.pfizer.com/news/press-release/press-release-detail/pfizer-declares-third-quarter-2025-dividend

- https://finance.yahoo.com/news/3-reasons-pfizer-stock-could-134500491.html

- https://www.pfizer.com/news/press-release/press-release-detail/pfizer-provides-full-year-2025-guidance-and-reaffirms-full

- https://investingnews.com/pfizer-declares-third-quarter-2025-dividend/

- https://www.morningstar.com/stocks/xnys/pfe/quote

- https://www.investors.com/news/technology/pfizer-stock-buy-now/

- https://www.moneycontrol.com/markets/financials/quarterly-results/pfizer-p/

- https://finance.yahoo.com/quote/PFE/

- https://www.marketbeat.com/instant-alerts/pfizer-nysepfe-stock-price-expected-to-rise-bank-of-america-analyst-says-2025-10-03/

- https://www.pfizerltd.co.in/financial-information

- https://www.zacks.com/stock/news/2761564/is-pfe-stock-a-buy-after-14-rise-post-drug-pricing-deal-with-trump

- https://www.cnn.com/markets/stocks/PFE

- https://investors.pfizer.com/Investors/Financials/Quarterly-Results/

- https://services.thebmc.co.uk/bullish-on/Why-analysts-maintain-buy-rating-on-PFE-stock

- https://finance.yahoo.com/quote/PFE/analysis/

- https://investors.pfizer.com/Investors/Financials/Annual-Reports/default.aspx