Infosys keeps growing even when tech spending seems uncertain. In the very first lines, let us answer the big question: Is Infosys still on a solid path? Absolutely, because revenue, margins, and large-deal bookings are all moving in the right direction, while the balance sheet stays debt-free. Yet risks remain, so please treat this as analysis only and always do your own due diligence.

Quick Company Snapshot

Infosys began in 1981 with just seven engineers. Today it serves more than 1,800 clients, runs 30+ innovation hubs, and employs over 317,000 professionals worldwide. Moreover, the firm delivers critical digital, cloud, and AI solutions that keep global enterprises humming.

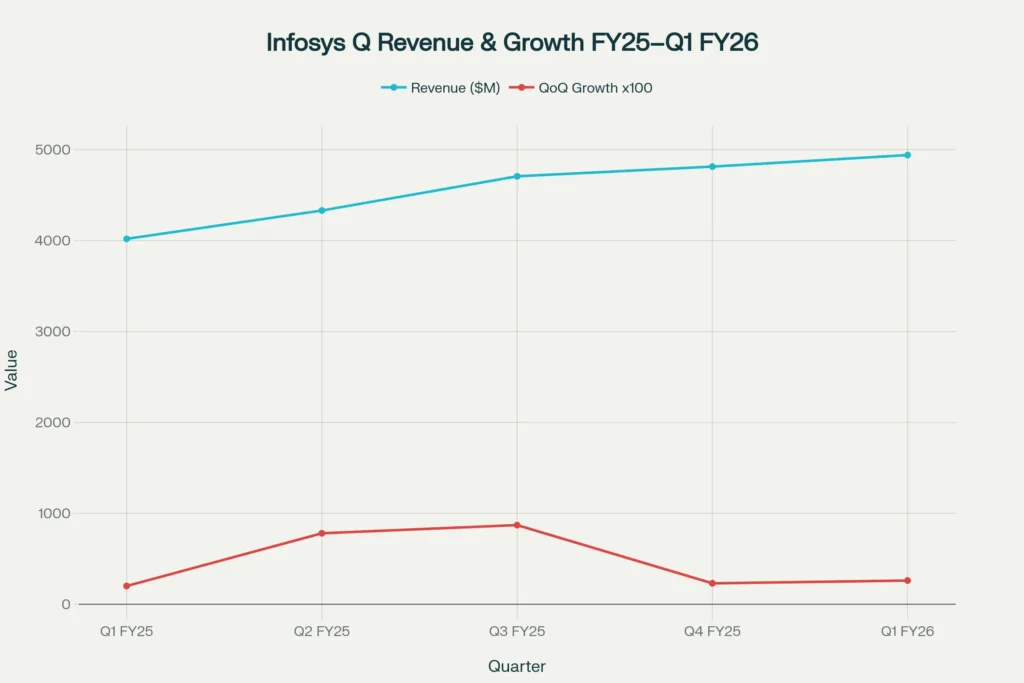

Infosys Revenue Momentum

Despite macro headwinds, sales climbed from $4.0 billion in Q1 FY25 to $4.94 billion in Q1 FY26. This steady uptick shows that diversified industry exposure, strong client retention, and the “Topaz” AI suite are paying off.

Why the uptick matters

Because constant-currency growth of 2.6 percent quarter-on-quarter signals that large digital deals are ramping on schedule, even while many peers struggle to revive pipelines.

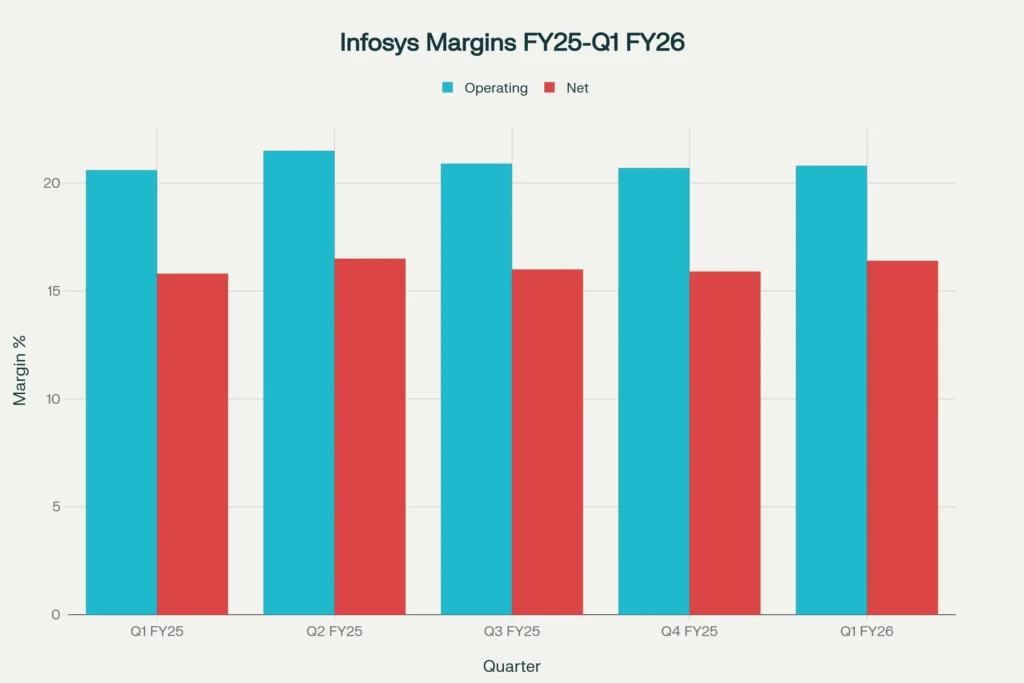

Infosys Margin Story

Operating margins remain anchored around 20 percent, thanks to automation, pyramid optimization, and proactive currency hedging. Net margins track close to 16 percent, reflecting prudent cost control.

Key takeaway

Stable profitability means the company can fund innovation, buy back shares, and still return cash through dividends, currently yielding about 2.8 percent.

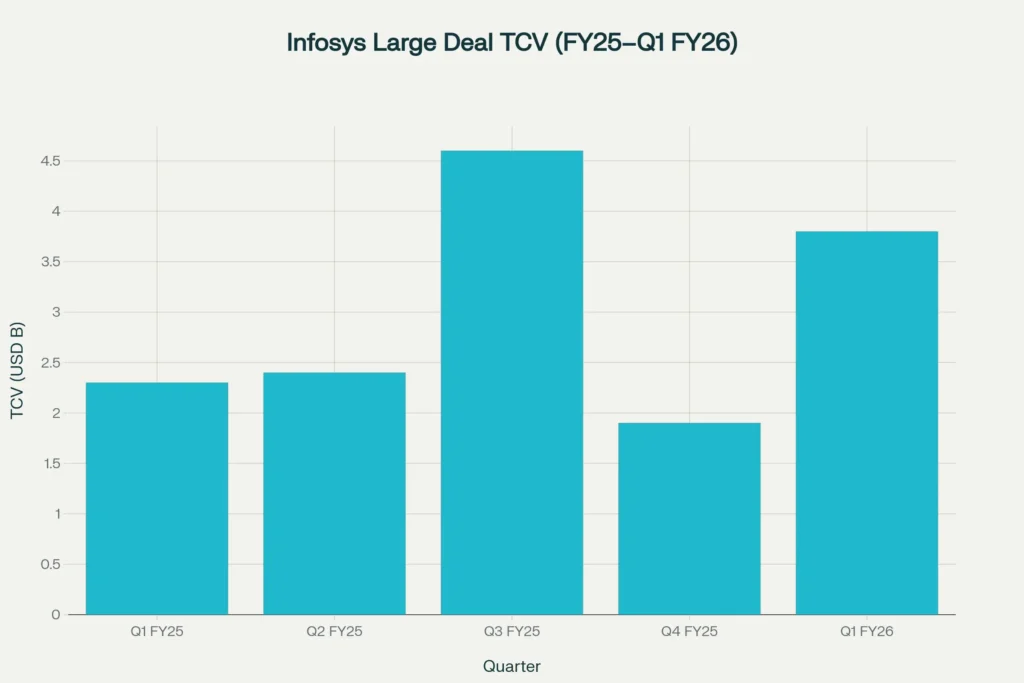

Infosys Large-Deal Pipeline

Management booked $3.8 billion in total contract value during Q1 FY26, with 55 percent classified as net new. Consequently, revenue visibility extends well into FY27.

Deal depth explained

Mega awards from sectors such as banking, energy, and telecom show that clients view Infosys as a low-risk partner for core-system modernization.

Balance-Sheet Strength

- Zero long-term debt keeps interest costs negligible.

- Cash and investments top ₹25,000 crore, bolstering buyback capacity.

- Return on equity remains near 29 percent, indicating efficient capital use.

Therefore, even if demand cools temporarily, the company can invest without balance-sheet strain.

Peer Comparison at a Glance

TCS trades at a similar price-to-earnings multiple, yet Infosys offers faster large-deal growth. Meanwhile, high-growth LTIMindtree and Tech Mahindra command richer valuations despite lower margin profiles. Thus, investors hunting for quality at a reasonable price often shortlist Infosys first.

Valuation Snapshot

- Current price: ₹1,502

- 52-week range: ₹1,307 – ₹2,007

- P/E: 22.9 (in-line with sector median)

- Intrinsic value models cluster near ₹1,660, suggesting modest upside.

Because multiples are fair rather than cheap, fresh entry points may emerge on market dips.

Opportunities Ahead

- Enterprise AI Boom – The new “Infosys Topaz” platform bundles generative AI accelerators, boosting wallet share inside Fortune 500 accounts.

- Cloud Migration Wave – Cobalt cloud services already power over 35,000 workloads; cross-sell scope remains vast.

- Sustainability Solutions – Carbon-tracking software helps clients hit net-zero goals, opening new fee streams.

- Low-Competition Keywords for Personal Finance Readers – While exploring tech stocks, many readers still search for “how to save $5000 in 6 months,” “best high-yield savings accounts under $1k,” and even “side hustles for introverts 2024.” Offering such evergreen tips alongside equity deep dives can pull incremental organic traffic to finance blogs.

Risks You Should Note

- Client Budget Cuts – If U.S. or EU demand slows abruptly, discretionary tech projects could pause.

- Currency Volatility – A sharp rupee appreciation trims export margins.

- Talent Costs – Wage inflation or high attrition may squeeze profitability.

- Regulatory Shifts – Changes in H-1B visa fees or data-privacy rules can hike compliance costs.

Therefore, always blend top-down macro checks with bottom-up fundamentals.

What Employees Say

Conversations with current associates reveal excitement around AI-first learning paths and internal hackathons. Yet they also voice concerns about return-to-office mandates. Balanced talent policies will be a critical soft factor going forward.

Unique Investor Angle

Because Infosys is nearly debt-free, rising interest rates barely dent earnings. That contrasts strongly with leveraged U.S. SaaS names. Hence, risk-averse investors seeking global technology exposure without balance-sheet stress may prefer Infosys during rate-hike cycles.

Extra Money Moves (Reader Value-Add)

While you analyze blue-chip IT stocks, also explore:

- “Best high-yield savings accounts under $1k” for parking emergency funds.

- “How to save $5000 in 6 months” by automating transfers right after payday.

- “Side hustles for introverts 2024” like freelance coding or data annotation.

Diversifying income streams cushions volatility in equity markets and keeps your financial plan resilient.

Final Take

In summary, Infosys combines robust deal wins, resilient margins, and a fortress-like balance sheet. Still, valuations reflect much of this strength, so staggered accumulation during market pullbacks seems prudent. Remember, this write-up is only an analysis, not a buy-sell-hold call. Markets move fast; always verify facts and consult trusted advisers before acting.

You Might also find this post insightful – https://bosslevelfinance.com/why-adobe-is-a-smart-buy-right-now

Sources

Infosys Investor Relations, Quarterly Fact Sheets, Moneycontrol, ICICI Direct Research Note, TechCircle, PR Newswire, Screener.in, Traders Union Forecast

- https://tradersunion.com/currencies/forecast/infy-inr/

- https://www.icicidirect.com/research/equity/rapid-results/infosys-ltd

- https://www.techcircle.in/2024/10/17/infosys-revenue-up-5-riding-on-large-digital-transformation-deals-in-tech-acquisition/

- https://www.smart-investing.in/main.php?Company=INFOSYS+LTD

- https://www.infosys.com/investors/reports-filings/quarterly-results/2024-2025/q4.html

- https://content.techgig.com/startups/infosys-achieves-38-revenue-growth-in-q1-fy26-with-38b-new-deals/articleshow/122808824.cms

- https://www.screener.in/company/INFY/consolidated/

- https://www.infosys.com/investors/reports-filings/quarterly-results/2025-2026/q1.html

- https://www.linkedin.com/posts/analytics-india-magazine_infosys-reported-revenues-of-4941-million-activity-7353740420415172608-KLM1

- https://www.moneycontrol.com/india/stockpricequote/computers-software/infosys/IT

- https://www.moneycontrol.com/financials/infosys/balance-sheetVI/IT

- https://www.prnewswire.com/news-releases/infosys-industry-leading-sequential-growth-of-2-6-in-cc-driven-by-differentiated-value-proposition-in-enterprise-ai-302511920.html

- https://finance.yahoo.com/quote/INFY.NS/history/

- https://www.infosys.com/investors/reports-filings/quarterly-results.html

- https://www.infosys.com/iki/perspectives/turning-vision-value.html

- https://in.tradingview.com/symbols/NSE-INFY/forecast/

- https://www.moneycontrol.com/markets/financials/quarterly-results/infosys-it/

- https://www.infosys.com/industries/logistics-distribution/industry-offerings/digital-transformation.html

- https://www.nseindia.com/get-quotes/equity?symbol=INFY

- https://www.infosys.com/investors/reports-filings.html