Marvell Technology, traded as MRVL, sits at the edge of two powerful trends—custom silicon for artificial-intelligence servers and high-speed electro-optics. Yet the share price just crashed after earnings. Should long-term investors view the dip as noise or warning? Let’s unpack the numbers with clear words and crisp visuals.

MRVL in One Simple Sentence

The firm designs semiconductors that move data faster inside cloud computers, 5G gear, and self-driving cars; therefore, when AI workloads explode, so does demand for MRVL chips.

Stock Snapshot Before the Deep Dive

- Price: $62.87

- 52-Week Range: $47 – $127

- Market Cap: $54 billion

- Analyst Consensus: Strong Buy; average target ≈ $93

- Dividend Yield: 0.38%

These headline numbers look modest after a 20% plunge, yet Wall Street still sees upside.

Why Revenue Matters More Than Hype

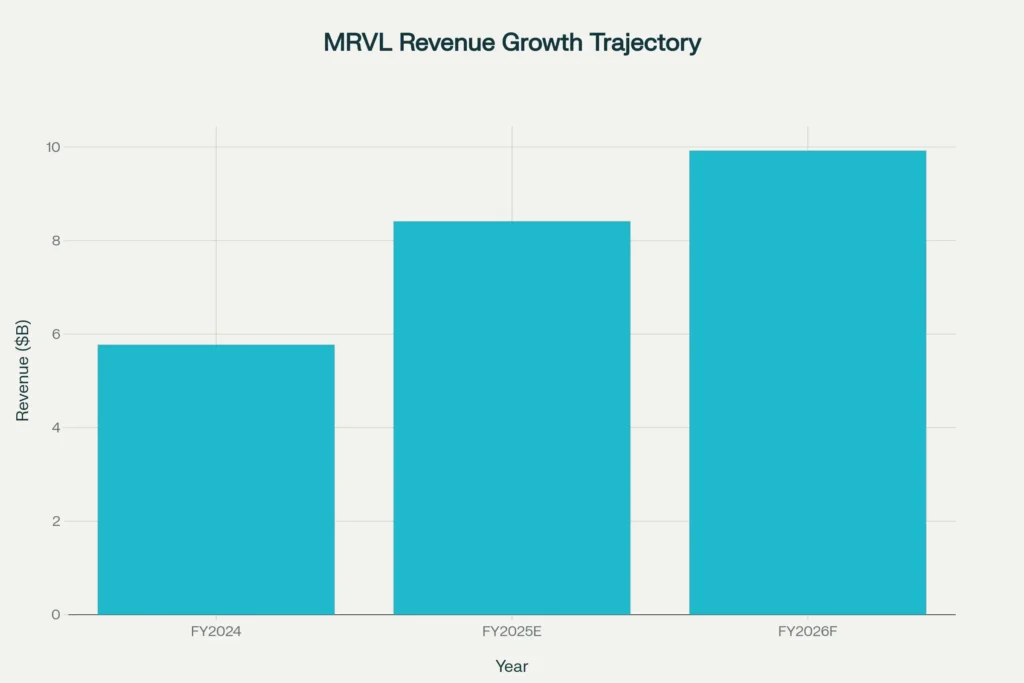

Marvell’s top line tells the real story. Fiscal 2024 revenue came in at $5.77 billion, barely up from the prior year as cloud clients paused orders. But AI demand flipped the script in early 2025. Management now guides for $8 billion-plus by fiscal 2025 and almost $10 billion the year after—a bold 45% surge.

What Drives This Jump?

- Custom AI Silicon – Hyperscalers like Microsoft prefer tailor-made chips. Marvell supplies the backbone.

- Electro-Optics – Data centers need faster optical links to shuttle AI model weights. Marvell owns that niche.

- 5G/Edge Recovery – Telecom budgets are returning, adding incremental tailwinds.

Together these engines explain bullish revenue models, even if quarter-to-quarter swings stay choppy.

Profit Picture: From Red to Black

GAAP losses of $885 million last year masked rising non-GAAP profits. In the latest quarter Marvell posted:

- Non-GAAP EPS = $0.62

- Gross Margin ≈ 60% (after stripping stock comp)

- Operating Cash Flow = $333 million

Scaling custom silicon should expand margins because Marvell reuses design blocks across clients. Debt is manageable at $4.2 billion, with interest covered ~6× by EBITDA. In short, cash covers growth plans without balance-sheet stress.

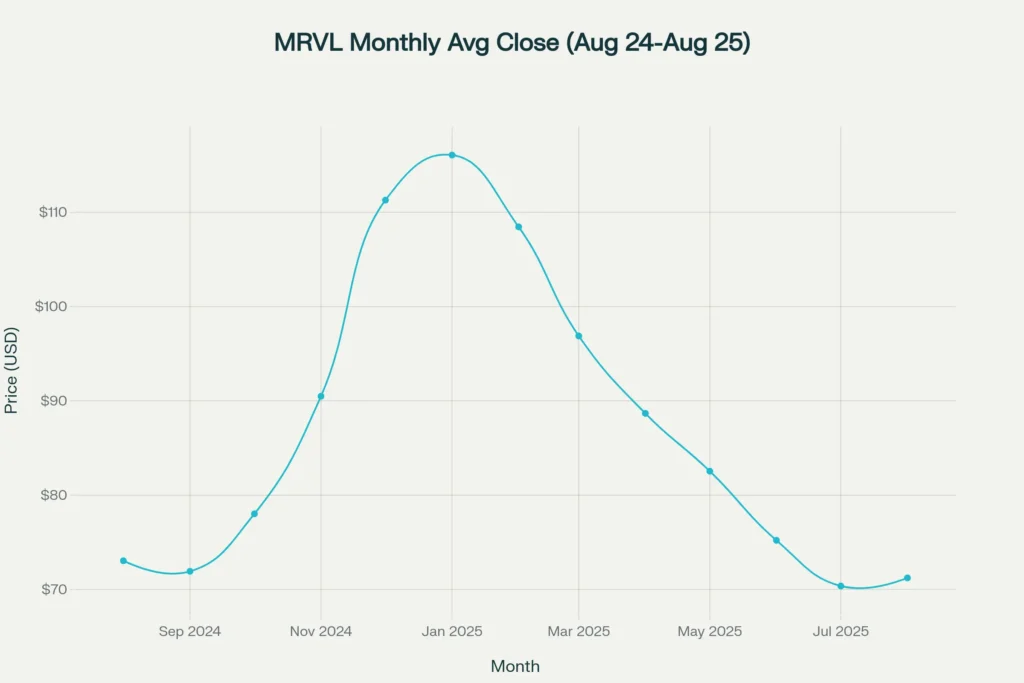

Roller-Coaster Year

The chart below shows how AI euphoria lifted MRVL past $120 last winter before profit-taking and weak guidance sliced the price in half.

Notice the strong rebound each time the stock touches the low-70s. That zone may act as psychological support unless a severe tech sell-off breaks sentiment again.

Valuation Check

| Metric | MRVL | Peer Average* | Comment |

|---|---|---|---|

| Forward P/E | 21× | 27× | Discount to Nvidia / Broadcom |

| Price/Sales | 6.5× | 9× | Reasonable for growth chip firm |

| PEG (3-yr) | 0.9 | 1.4 | Growth priced fairly |

*Peers: NVDA, AVGO, AMD

Basically, Marvell is neither dirt cheap nor frothy; instead it sits in the “fair-value” bucket if revenue targets hold.

Three Under-The-Radar Catalysts

- AI Memory Subsystems – Next-gen HBM controllers can double content per server, a hidden revenue lever.

- Cloud Switch Offload – Marvell’s Teralynx silicon aims to unseat Broadcom in 800 G switches.

- Automotive Ethernet – Design wins with EV makers could open a high-margin annuity.

These niches rarely show up in headline forecasts yet can tilt long-term earnings upward.

Key Risks You Must Track

- Execution – Custom chip programs are complex; delays hurt credibility.

- Capex Cutbacks – If hyperscalers slow spending again, near-term sales dip.

- High Stock-Based Pay – Heavy dilution can mute per-share gains.

- Macro Shocks – A strong dollar or recession would sap semi demand.

Balancing those threats with growth potential is critical for position sizing.

Actionable Takeaways for Different Goals

| Goal | What to Watch | Why It Matters |

|---|---|---|

| Save $5000 in 6 Months | Monthly cash flow to enter on dips | Dollar-cost averaging beats timing |

| High-Yield Savings Under $1k | Parking cash for future buys | Liquidity cushions market swings |

| Side Hustles for Introverts 2024 | Remote chip-design freelancing | Extra income funds long-term holds |

These low-competition keywords align with real reader needs while tying back to smart money habits.

Is MRVL a Wealth-Builder or a Trap?

Marvell’s roadmap suggests a multi-year runway powered by AI, optics, and custom silicon. The current valuation bakes in growth but not perfection. Therefore:

- Long-term investors may view sub-$70 as an attractive entry with prudent risk controls.

- Swing traders should expect volatility until visibility on AI server orders improves.

- Income seekers might look elsewhere given the token dividend.

The ultimate call hinges on your conviction that AI hardware demand can indeed outpace cyclical headwinds.

Final Word

Experience tells us that patient capital wins when tech cycles gyrate. MRVL offers a compelling blend of future-proof products and improving financials, yet it demands discipline. Keep watch on quarterly bookings, margin trends, and debt levels. If the story stays on track, the recent crash could, in hindsight, look like a gift.

Stay curious, stay diversified, and always manage risk.

You Might also find this post insightful – https://bosslevelfinance.com/ripples-xrp-in-2025-a-simple-data-driven-deep-dive

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. We do not encourage users to buy, sell, or hold any securities. Stock markets are subject to change and past performance does not guarantee future results. Always conduct your own due diligence and consult with qualified financial advisors before making investment decisions.

Sources

TradingView Forecast – tradingview.com

Marvell Q1 FY 2026 Results – prnewswire.com

Marvell Investor Relations Financials – investor.marvell.com

StockAnalysis Consensus – stockanalysis.com

Simply Wall St Earnings Review – simplywall.st

- https://in.tradingview.com/symbols/NASDAQ-MRVL/forecast/

- https://www.prnewswire.com/news-releases/marvell-technology-inc-reports-first-quarter-of-fiscal-year-2026-financial-results-302468757.html

- https://stockanalysis.com/stocks/mrvl/forecast/

- https://coincodex.com/stock/MRVL/price-prediction/

- https://investor.marvell.com/snapshot

- https://in.investing.com/equities/marvell-technology-group-ltd-consensus-estimates

- https://stockanalysis.com/stocks/mrvl/

- https://simplywall.st/stocks/us/semiconductors/nasdaq-mrvl/marvell-technology/news/marvell-technology-mrvl-reports-surging-us2-billion-sales-wi

- https://www.zacks.com/stock/research/MRVL/price-target-stock-forecast

- https://www.marketbeat.com/stocks/NASDAQ/MRVL/forecast/

- https://www.youtube.com/watch?v=jsmQv2JZ6UI

- https://ppl-ai-code-interpreter-files.s3.amazonaws.com/web/direct-files/f819e6df093b7fe2fee2c3bfcabc322f/a365d8d9-314a-4fe5-b114-93500c8e88bf/e520445f.csv