Understanding This LIC-Owned Banking Giant

The Life Insurance Corporation owns 94.71% of this major bank (IDBI Bank). Furthermore, this unique ownership structure provides stability during tough times. Additionally, the government support creates confidence among investors.

Moreover, this financial institution operates across India with thousands of branches. Also, it serves millions of customers through various banking products. Furthermore, the bank focuses on both retail and corporate banking segments.

Currently, the stock trades at ₹85.67 with a market cap of ₹92,137 crores. Additionally, it pays a dividend yield of 2.41%. Similarly, the book value stands at ₹57.3 per share.

Financial Performance Shows Strong Growth

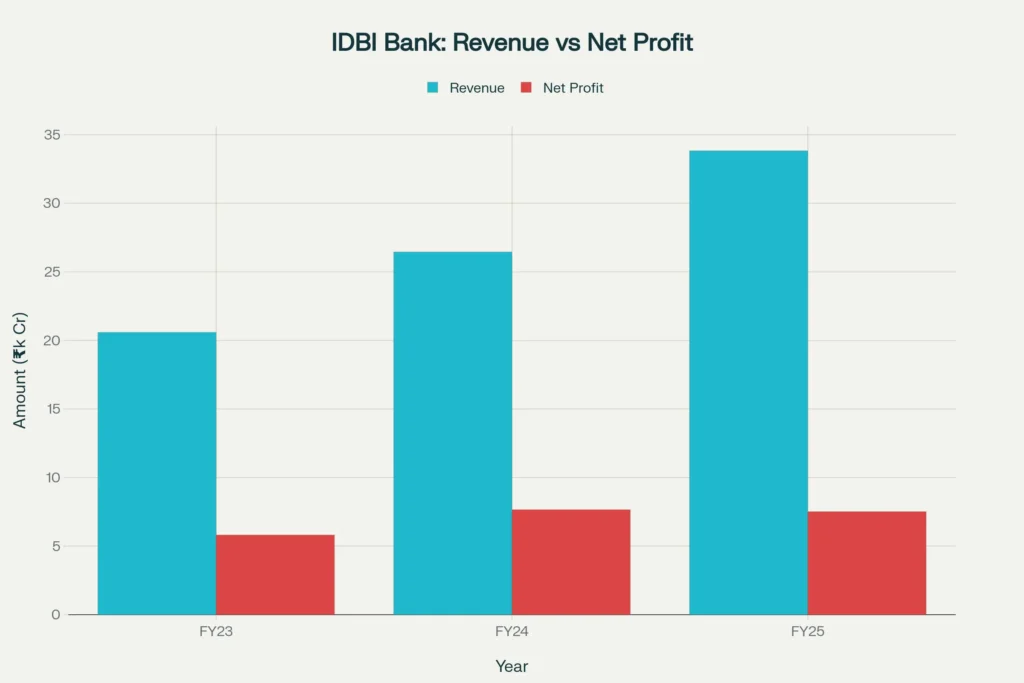

The company delivered impressive profit growth over recent years. Moreover, net profit increased 26% to ₹2,051 crores in Q4 FY25. Furthermore, total income rose to ₹33,826 crores during FY25.

Additionally, the bank’s revenue growth has been consistent. Similarly, operating efficiency improved across quarters. Moreover, net interest margins expanded to 5.17% in December 2024.

However, profit margins faced some pressure recently. Yet, the overall trend remains positive. Furthermore, management maintains disciplined cost control.

Asset Quality Improvement Tells The Real Story

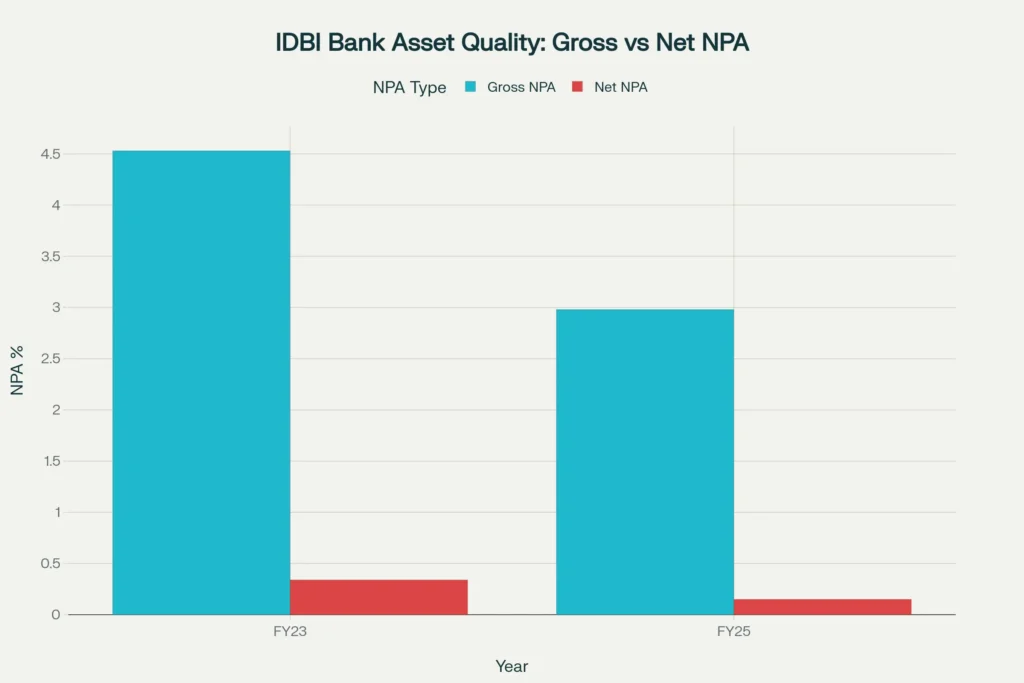

The bank’s asset quality showed remarkable improvement. Moreover, gross non-performing assets dropped to 2.98% in March 2025. Additionally, net NPAs fell dramatically to just 0.15%.

Similarly, provisioning requirements decreased significantly. Furthermore, the bank recovered more bad loans than expected. Also, credit risk management improved across all segments.

Moreover, retail advances grew 18% year-over-year. Additionally, corporate lending picked up momentum. Furthermore, the loan portfolio diversification reduced concentration risks.

Valuation Metrics Point to Opportunity

The stock trades at a P/E ratio of 11.6, which is reasonable. Moreover, the price-to-book ratio of 1.69 suggests fair valuation. Additionally, dividend yield of 2.34% attracts income investors.

Furthermore, return on equity improved to 14% last year. Similarly, return on assets reached 1.99%. Moreover, these metrics compare well with industry peers.

However, investors should watch interest coverage ratios closely. Yet, overall profitability trends remain encouraging. Additionally, capital adequacy ratios stay above regulatory requirements.

LIC Divestment Creates Unique Opportunity

The government plans to sell its stake through LIC. Moreover, this divestment process is progressing smoothly. Additionally, qualified bidders completed due diligence recently.

Furthermore, financial bids are expected by December quarter. Similarly, winning bidders should emerge by fiscal end. Moreover, this process may unlock value for shareholders.

However, regulatory approvals may take time. Yet, market participants remain optimistic. Additionally, the new ownership structure could improve efficiency.

Technical Analysis Shows Mixed Signals

The stock hit a 52-week high of ₹106.32 earlier. Moreover, it recently found support near ₹65.89. Additionally, current levels offer reasonable entry points for long-term investors.

Furthermore, trading volumes remain healthy during market sessions. Similarly, institutional interest continues across quarters. Moreover, retail participation has increased recently.

However, short-term momentum appears weak. Yet, long-term charts show upward bias. Additionally, key support levels hold during corrections.

Risk Factors Worth Considering

Banking stocks face interest rate risks always. Moreover, economic slowdowns affect loan growth significantly. Additionally, regulatory changes can impact profitability quickly.

Furthermore, asset quality concerns may resurface during downturns. Similarly, competition from fintech companies increases constantly. Moreover, digitalization requires continuous investments.

However, government backing provides stability during crises. Yet, management execution remains crucial for success. Additionally, market conditions affect all banking stocks similarly.

Investment Strategy for Different Investor Types

Conservative investors may find dividend yields attractive here. Moreover, systematic investment plans can reduce volatility risks. Additionally, long-term holding periods suit this stock best.

Furthermore, value investors see opportunity at current levels. Similarly, dividend-focused portfolios benefit from consistent payouts. Moreover, institutional ownership provides confidence during corrections.

However, growth investors may prefer other alternatives. Yet, turnaround stories often deliver superior returns. Additionally, patient capital gets rewarded eventually.

Long-term Outlook Remains Positive

The banking sector outlook appears encouraging overall. Moreover, economic growth drives loan demand naturally. Additionally, digital banking adoption creates new opportunities.

Furthermore, government infrastructure spending benefits banks directly. Similarly, rural credit demand continues growing steadily. Moreover, financial inclusion initiatives support long-term growth.

However, global economic uncertainties remain present. Yet, domestic demand drivers stay intact. Additionally, regulatory support continues for the sector.

You Might also find this post insightful – https://bosslevelfinance.com/jk-paper-stock-what-investors-must-know-now

Important Disclaimer: This analysis is for educational purposes only. We do not encourage users to buy, sell, or hold any stocks. Stock markets are subject to change and all investments carry risks. Please do your own due diligence and consult qualified financial advisors before making any investment decisions.

Sources:

- Screener.in – IDBI Bank Financial Data

- Business Standard – Q4FY25 Results Analysis

- Moneycontrol – Stock Price Information

- Groww – Financial Statements Data

- Tickertape – Market Metrics

- ICICI Direct – Company Overview

- IDBI Bank Official Investor Presentation

- Investing.com – Consensus Estimates

- https://www.screener.in/company/IDBI/consolidated/

- https://www.business-standard.com/companies/quarterly-results/idbi-bank-q4fy25-results-net-profit-increases-26-to-2-051-crore-125042800684_1.html

- https://walletinvestor.com/bse-stock-forecast/idbi-bank-ltd-bse-prediction

- https://www.moneycontrol.com/india/stockpricequote/bank-private/idbibank/IDB05

- https://groww.in/stocks/idbi-bank-ltd/company-financial

- https://www.tickertape.in/stocks/idbi-bank-IDBI

- https://www.icicidirect.com/stocks/idbi-bank-ltd-share-price

- https://www.idbibank.in/pdf/Analyst_Dec_2024.pdf

- https://in.investing.com/equities/idbi-bank-consensus-estimates

- https://sewamitra.up.gov.in/sensitivity-analysis/IDBI-Bank-Limited-Stock-Analysis:-Technical-Signals-for-2025