Why Starbucks Still Sits at the Top

Starbucks built a global café culture—and, importantly, a cash-rich business—by blending premium coffee with a digital edge. Moreover, the brand’s 41,000-plus locations generate a steady river of cash even when consumer moods shift. Therefore, investors watch every earnings call for clues about traffic, ticket size, and new menu magic.

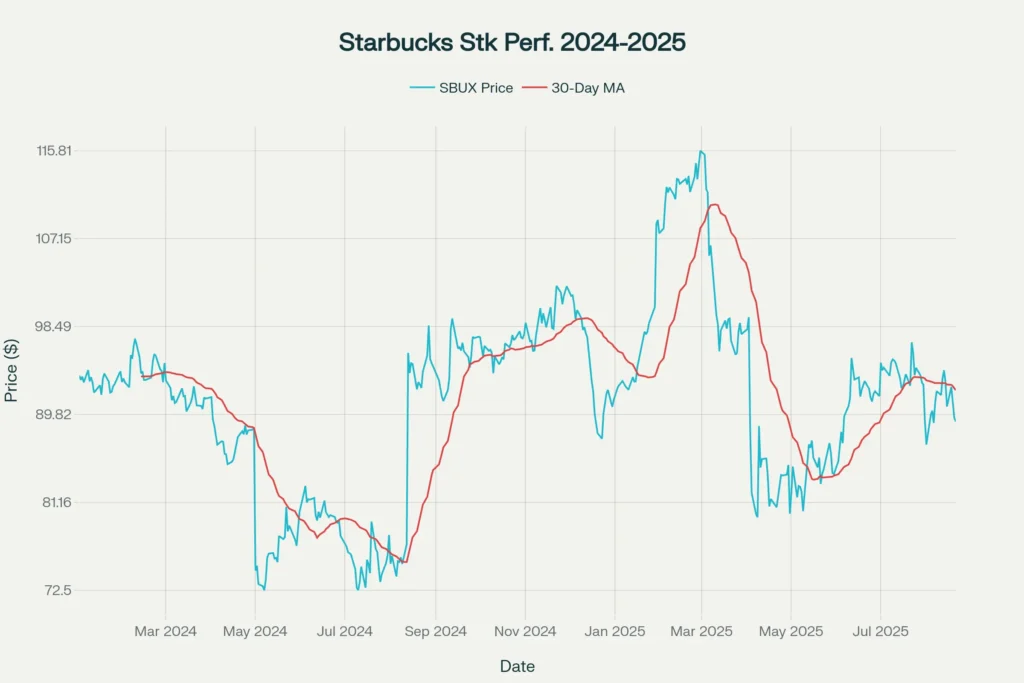

Starbucks Price Action: Story in Two Lines

The share price bounced strongly in early 2024, cooled when earnings disappointed, yet still rides a long-term uptrend. The 30-day moving average helps us see that underlying trend.

What the Chart Tells Us

Because the moving average slopes upward, long-term momentum remains intact. However, recent dips warn that volatility can return fast—especially when earnings miss lofty forecasts.

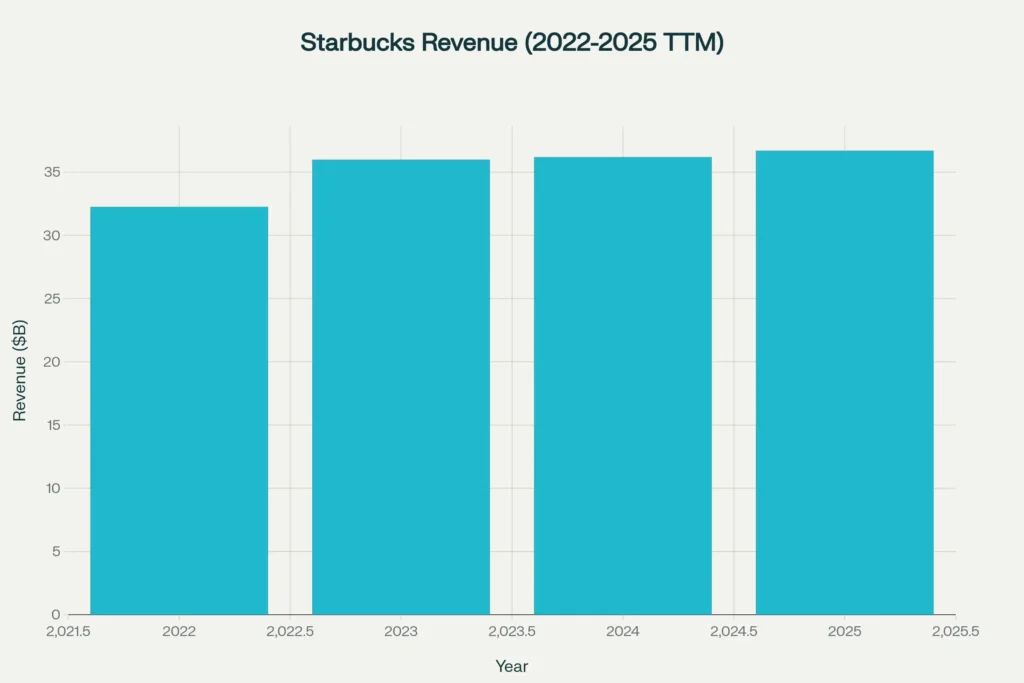

Starbucks Revenue Keeps Brewing

Even in a choppy consumer climate, yearly top-line growth continues, though at a slower drip. The bar chart below highlights a steady climb toward new highs.

Reading the Bars

Revenue rose from $32 billion in 2022 to $36.7 billion over the last twelve months. Although the pace slowed, the brand still eked out gains while many discretionary names posted declines.

How the Business Makes Money

1. North America Stores (71% of sales)

This core arm serves loyal U.S. customers who embrace mobile ordering and rewards. Because digital orders carry higher tickets, mix shifts can boost margins even when traffic dips.

2. International Stores (25%)

China remains the crown jewel. Yet, economic softness trimmed average tickets there last quarter. Even so, China’s net new stores will likely outpace the U.S. for years.

3. Channel Development & Licensing (4%)

Packaged coffee, ready-to-drink bottles, and grocery pods create royalty streams that feel almost “set and forget.” This segment cushions earnings when café traffic slows.

Fundamental Health Check

| Metric (FY 2025 Q3) | Value | Trend |

|---|---|---|

| Net Revenue | $9.5 B | +4% YoY |

| GAAP EPS | $0.49 | −45% YoY |

| Operating Margin | 10.1% | −6.5 ppt YoY |

| Global Stores | 41,097 | +6% YoY |

Although revenue inched higher, margins shrank due to wage hikes, supply costs, and a “Back to Starbucks” investment plan. Therefore, profitability remains the key lever to watch.

Starbucks Growth Engines

Digital Rewards Flywheel

The U.S. program now boasts 34 million active members. Each member spends more, visits more often, and anchors the brand against cheaper rivals.

Drive-Thru 2.0

New prototype stores use compact footprints and faster lanes, aiming to trim build costs by 10% while boosting throughput by 20%.

Menu Simplification

Cutting 30% of low-selling items frees space for high-margin cold beverages and seasonal hits—think Pumpkin Spice with protein cold foam.

Risks Roasting Under the Lid

- Sluggish Comparable Sales

Two consecutive quarters of negative comps show price hikes alone cannot offset lower footfall forever. - Wage Inflation

Starbucks pledged $500 million in partner investments. While good for morale, the spend squeezes margins if traffic fails to rebound. - China Uncertainty

Youth unemployment and cautious consumers hurt ticket sizes. Any geopolitical shock could disrupt the most important international market. - Union Push

Labor activism adds costs and complicates store-level scheduling. Investors should monitor how wage negotiations evolve.

Actionable Investor Checklist

- Track Margin Recovery – A move back toward 15% operating margin would signal the turnaround is working.

- Watch China Tickets – Even a small uptick in average spend could swing earnings meaningfully.

- Follow Store Economics – New drive-thru builds must prove they lower cap-ex and lift returns.

- Monitor Rewards Growth – Digital engagement often predicts traffic three-to-six months out.

Final Sip: Should Investors Stay Awake?

Starbucks blends brand power, digital loyalty, and global expansion. Although earnings wobble, free cash flow stays hot enough to fund dividends and buybacks. Because valuation now sits near the five-year average P/E, some investors may view the recent dip as a refill opportunity—provided they can stomach near-term volatility.

You Might also find this post insightful – https://bosslevelfinance.com/the-ethereum-2025-upgrade-powering-digital-finance-growth

Disclaimer

This post is only analysis. It does not urge readers to buy, sell, or hold Starbucks shares. Markets shift quickly. Always perform your own research and consult qualified professionals.

Source Links

- Starbucks Q3 FY 2025 earnings release (PDF)

- Nasdaq press release on Q3 2025 results

- Macrotrends Starbucks revenue data

- Statista global store count 2024

- Investor.starbucks.com Q2 FY 2025 release

- Statista regional store breakdown 2024

- World Population Review store counts 2025

- https://s203.q4cdn.com/326826266/files/doc_financials/2025/q3/SBUX-06-29-2025-Exhibit-99-1-1.pdf

- https://www.statista.com/statistics/218366/number-of-international-and-us-starbucks-stores/

- https://www.nasdaq.com/press-release/starbucks-reports-q3-fiscal-year-2025-results-2025-07-29

- https://s203.q4cdn.com/326826266/files/doc_financials/2025/q2/SBUX-3-30-2025-Exhibit-99-1.pdf

- https://www.statista.com/statistics/266465/number-of-starbucks-stores-worldwide/

- https://in.investing.com/news/transcripts/earnings-call-transcript-starbucks-q3-2025-misses-eps-forecast-revenue-beats-93CH-4933261

- https://www.linkedin.com/pulse/starbucks-q2-fiscal-year-2025-performance-analysis-072925-amjad-htsvf

- https://worldpopulationreview.com/country-rankings/starbucks-stores-by-country

- https://news.alphastreet.com/sbux-earnings-starbucks-q3-2025-profit-falls-despite-higher-revenues/

- https://macrotrends.net/stocks/charts/SBUX/starbucks/revenue

- https://www.stonex.com/en/market-intelligence/coffee/202501291413/starbucks-reports-q1-fiscal-year-2025-results-global-store-sale/

- https://www.youtube.com/watch?v=HwULkunySFo

- https://investor.starbucks.com/news/financial-releases/news-details/2025/Starbucks-Reports-Q2-Fiscal-Year-2025-Results/default.aspx

- https://en.wikipedia.org/wiki/Starbucks